Silicon Carbide Market

Silicon Carbide Market - Global Industry Assessment & Forecast

214

2024

Nov - 2024

![]()

![]()

![]()

VMR-3223

Segments Covered

By

Product Type Black Silicon Carbide, Green Silicon Carbide, Other

By

Product Type Black Silicon Carbide, Green Silicon Carbide, Other

-

By

Device Type SiC Discrete Devices, SiC Power Modules, SiC Power Semiconductors, SiC Optoelectronic Devices

-

By

Application Power Electronics, Automotive, Renewable Energy, Industrial

-

By

End-Use Industry Automotive, Energy and Power, Electronics and Semiconductors, Aerospace and Defense, Other

-

By

Region North America, Europe, Asia Pacific, Latin America, Middle East & Africa

Snapshot

| 2024 | |

| 2025 - 2034 | |

| 2019 - 2023 | |

| USD 4.21 Billion | |

| USD 12.56 Billion | |

| 11.56% | |

| Asia Pacific | |

| Asia Pacific |

Customization Offered

Cross-segment Market Size and

Analysis

for Mentioned Segments

Cross-segment Market Size and

Analysis

for Mentioned Segments- Additional Company Profiles (Upto 5

With

No Cost)

- Additional Countries (Apart From

Mentioned Countries)

- Country/Region-specific Report

- Go To Market Strategy

- Region Specific Market Dynamics

- Region Level Market Share

- Import Export Analysis

- Production Analysis

- Others Request

Customization Speak To

Analyst

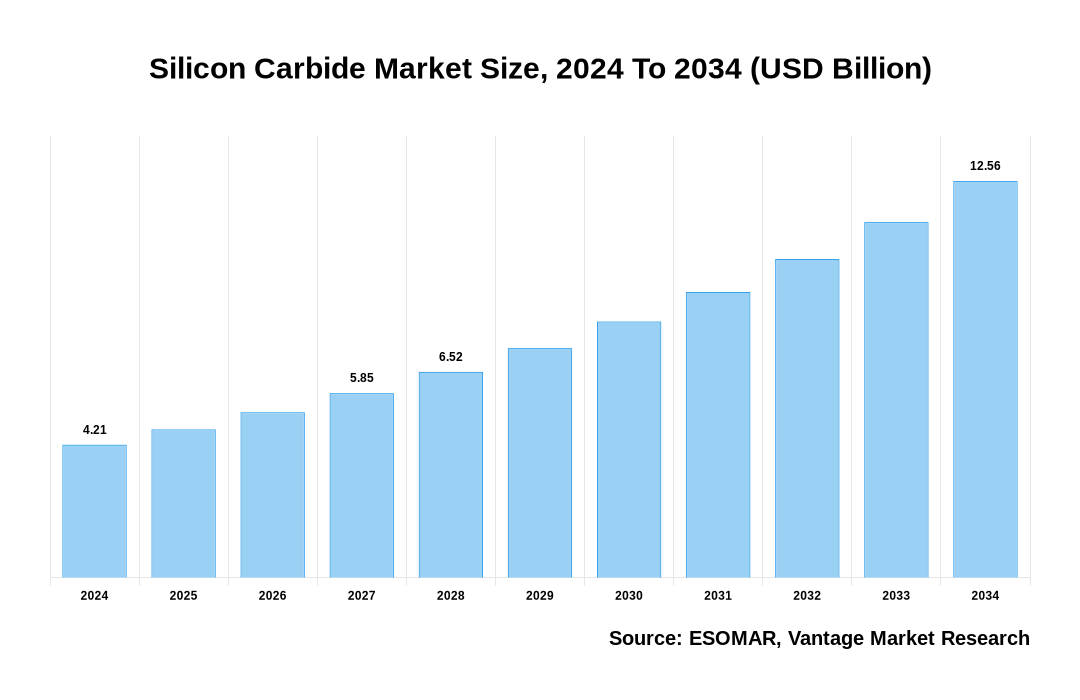

The global Silicon Carbide market size was USD 3.77 billion in 2023, and is calculated at USD 4.21 Billion in 2024. The market is projected to reach USD 12.56 Billion by 2034, and register a revenue 11.56% over the forecast period (2025-2034).

Premium Insights:

The global Silicon Carbide market revenue growth is driven by factors such as rising demand for Electric Vehicle (EV) power systems and solutions, advancements in power electronics, and expanding focus on renewable energy. High thermal conductivity, efficiency, and durability of SiC and increasing use in solar and wind energy infrastructure to improve power conversion is expected to support revenue growth of the market to a major extent. Silicon Carbide is widely used in the electronics sector, and black silicon carbide, green silicon carbide, coated Silicon Carbide is used for production of high temperature and high voltage components and devices, diodes, transistors, and sensors. Various components are proving crucial in deployment of 5G technology and infrastructure, and data centers due to thermal stability and high-frequency performance. Emerging applications span aerospace, laser radar systems, VUV telescopes, large astronomical telescopes, defense applications and equipment, and healthcare devices and equipment, where resilience of this material under extreme conditions is advantageous. Advancements in production techniques, such as 3D printing for SiC parts and components, along with improvements in wafer quality and fabrication technologies, are reducing costs and enhancing scalability. Moreover, innovations in material engineering and sustainable manufacturing practices are also expected to result in inclining demand from various sectors over the forecast period.

SiC is derived from silicon and carbon, and offers superior performance in high-stress, high-temperature environments. Silicon Carbide is a semiconductor, and is expected to replace other silicon-based semiconductors and transistors over time. Producing Silicon Carbidesubstrates begins with the creation of high-quality SiC crystals, making advancements in crystal growth techniques essential. Currently, popular methods for crystal growth include Vapor Phase Epitaxy (CVD) and Modified Liquid Phase Epitaxy (LPE).

Key end products, such as SiC-based power electronics, are widely used in electric vehicles, solar inverters, wind turbines, and high-voltage power systems, and serve to significantly improve energy conversion, efficiency, and durability. Also, SiC semiconductors are transforming sectors such as telecommunications, aerospace, and industrial manufacturing by delivering robust performance and reliability under extreme conditions. Major advantages of Silicon Carbideare high thermal conductivity and electric field resistance, which allows devices to operate at higher voltages and temperatures than traditional silicon-based solutions. These benefits are especially crucial in EVs and renewable energy infrastructure, where efficiency and longevity are critical.

Current trends include advancements in wafer production technology, such as the transition from 4-inch to larger 6-inch and 8-inch wafers, which is expected to increase manufacturing scale and reduce costs. Furthermore, ongoing research into 3D printing and other innovative SiC fabrication methods shows promise for reducing production costs and enabling more complex designs. As industries increasingly prioritize sustainability, the role of Silicon Carbide in energy-efficient systems is expected to expand, positioning it as a core material for green technology. This convergence of demand, technological advancement, and sustainability focus indicates a strong growth trajectory for the global Silicon Carbidemarket over the forecast period.

Silicon Carbide Market Size, 2024 To 2034 (USD Billion)

AI (GPT) is here !!! Ask questions about Silicon Carbide Market

Top Silicon Carbide Market Drivers and Trends:

- Expanding Electric Vehicle Market: The shift towards renewable energy and sustainable energy sources is driving up demand for EVS worldwide. This trend is having a major impact on demand for silicon carbide, owing to properties to improve energy efficiency and battery performance. Also, ability to handle high voltages and temperatures makes SiC essential in EV power modules, helping manufacturers meet the increasing performance and efficiency standards for green transportation.

- Renewable Energy and Power Electronics: High thermal conductivity and durability in adverse or harsh conditions make Silicon Carbide parts and components ideal for use in solar inverters, wind turbines, and power grids. As global initiatives push for cleaner energy, SiC-based systems are increasingly gaining traction to enhance reliability and efficiency of renewable energy infrastructure, and this trend is expected to continue to support growth of the market to a major extent.

- Technological Advancements in Manufacturing: Ongoing developments in wafer fabrication —transitioning from 4-inch to 6-inch and 8-inch wafers — and emerging techniques like 3D printing are improving scalability and cost-effectiveness of silicon carbide. These advancements reduce production costs, broaden application possibilities, and open avenues for new SiC-based innovations, thereby presenting additional opportunities for manufacturers to enhance competitiveness and revenue.

- Advancements in High-Performance Electronics: Rapid advancements in 5G technologies and infrastructure, high-power data centers, and advanced telecommunications are driving demand for SiC in electronics. Demand for SiC components continue to gain preference and use owing to reliability and performance in handling high frequencies and extreme temperatures, making them integral to the infrastructure of fast-evolving, high-performance industries.

Silicon Carbide Market Restraining Factor Insights

- High Production Costs: Silicon Carbide materials and components are costly to produce, largely due to complex manufacturing processes and the specialized equipment required for SiC wafer fabrication. While recent advancements are improving efficiency, scaling up production remains challenging. This high cost creates a barrier to adoption, especially in cost-sensitive industries where traditional silicon remains a viable, more affordable alternative.

- Limited Availability of High-Quality Raw Materials: The supply chain for SiC is constrained by limited access to high-purity raw materials and the need for precise, defect-free wafers. Achieving consistency in quality is both costly and time-intensive, often leading to delays in production and increased costs. This limitation hampers the growth potential of SiC across industries reliant on high-volume supply, such as automotive and electronics.

- Complex Manufacturing and Integration Challenges: Unique properties of Silicon Carbide necessitate specialized handling, which complicates integration into existing production systems. Industries may face technical hurdles when adapting SiC into their products due to different processing and assembly requirements compared to standard silicon. These integration challenges demand extensive research and development, increasing overall project costs and potentially delaying widespread adoption in the market.

Silicon Carbide Market Opportunities

- Strategic Partnerships and Agreements: Leading players in the Silicon Carbide (SiC) market can leverage opportunities to expand revenue by focusing on key sectors and strategic partnerships. Manufacturers can target the booming EV and renewable energy markets, by developing customized SiC solutions to optimize power efficiency in EVs, solar inverters, and wind turbines. By aligning with EV and green technology initiatives, companies can drive adoption and open lucrative, long-term revenue streams.

- Acquisitions and Mergers: Companies can increase market presence through mergers, acquisitions, and Joint Ventures (JVs). Collaborating with automotive and electronics firms allows for shared resources, expanded R&D capabilities, and faster scaling of SiC-based innovations.

- New Product Development: New product development tailored for high-performance sector such as 5G and aerospace presents an avenue for growth. By creating advanced, application-specific SiC components, manufacturers can cater to niche demand from industries with stringent performance needs. Adopting these strategies enables SiC manufacturers to not only boost revenue, but also strengthen position in pivotal future technologies.

Silicon Carbide Market Segmentation:

By Product Type:

- Black Silicon Carbide

- Green Silicon Carbide

- Other

By Device Type:

- SiC Discrete Devices

- Diodes

- MOSFETs

- SiC Power Modules

- SiC Power Semiconductors

- SiC Optoelectronic Devices

By Application:

- Power Electronics

- Automotive

- Electric Vehicles (EVs)

- Charging Infrastructure

- Renewable Energy

- Solar

- Wind

- Industrial

- Power Supplies

- Motor Drives

By End-Use Industry:

- Automotive

- Energy and Power

- Electronics and Semiconductors

- Aerospace and Defense

- Other

Segment Insights:

By Product Type:

In 2023, the green Silicon Carbide segment accounted for largest revenue share among the product type segments in the global Silicon Carbide market. Green SiC is preferred for its high purity and thermal resilience, and particularly suited for high-performance applications in electronics and energy sectors. Demand for green SiC is rising in power electronics and abrasive applications, where its hardness and thermal stability make it ideal for high-stress environments. Key trends indicate that as industries seek materials that can withstand extreme temperatures and enhance energy efficiency, green SiC will remain in demand, especially in applications requiring precision and durability over extended operational life.

By Device Type:

The SiC power modules segment accounted for largest revenue share among the device type segments in 2023 and this trend is expected to continue over the forecast period. These power modules play a critical role in electric vehicles and renewable energy infrastructure and offer high-efficiency power conversion, which is essential in extending EV range, improving battery performance, and reducing heat losses. With the rapid growth of EVs globally, as well as increased investments in fast-charging stations, the demand for SiC power modules is set to grow. Also, increasing utilization of SiC to improve the efficiency of solar inverters and wind power systems in renewable energy projects, where reliable high-voltage handling is a priority, is expected to continue to support revenue growth of this segment.

By Application:

The electric vehicles and charging infrastructure sub-segment of the automotive segments accounted for largest revenue share among the application segments in 2023. Silicon Carbide enables better power efficiency, higher driving range, and faster charging times, which are qualities and functionalities that are highly valued in EVs. With automakers investing substantially in EV technology and infrastructure, including ultra-fast charging networks, SiC is a preferred material for manufacturers aiming to optimize power management. As EV adoption accelerates globally, the role of Silicon Carbide in the automotive industry is expected to expand in parallel, and drive growth of this segment over the forecast period.

Report Coverage & Deliverables

Get Access Now

Track market trends LIVE & outsmart rivals with our Premium Data Intel Tool: Vantage Point

By End-User Industry:

Among the end-use industry segments, the automotive segment is expected to lead in terms of revenue share over the forecast period. Factors such as rising demand for electric vehicles and the need for high-efficiency power systems, coupled with rising focus on sustainable practices and reducing carbon emissions in the automotive sector, which align with the benefits offered by SiC technology, are expected to support revenue growth of this segment. The ongoing shift toward electrification in transportation also highlights the need for automotive manufacturers to shift towards advanced materials like SiC to improve vehicle performance and energy efficiency. Also, rising investments in EV infrastructure and production ramp up will certainly enhance the significance of Silicon Carbide in the automotive industry.

Regions and Countries

North America

- United States

- Canada

- Mexico

Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

Asia Pacific

- China

- Japan

- India

Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

Rest of Latin America

- Middle East & Africa

- Saudi Arabia

- South Africa

- United Arab Emirates

- Israel

- Rest of MEA

Silicon Carbide Market Regional Landscape:

Among the regional markets in 2023, Asia Pacific Silicon Carbidemarket accounted for largest revenue share of over 60% of global market revenue and is expected to register faster revenue growth rate over the forecast period. Factors such as robust manufacturing sector, rising electric vehicle (EV) production, and extensive electronics industry can be attributed to this majority share. Countries contributing significantly to revenue growth include China, Japan, and South Korea, owing to high demand for SiC components, and increasing investments in EV technology, power electronics, and renewable energy infrastructure.

The North America market accounted for second-largest revenue share in the global market in 2023, with the US leading in terms of revenue share contribution. Growth of the market in the US is driven by rising adoption of SiC in EVs and steady push for efficient energy solutions in power grids and renewable projects, advancements in 5G networks, and industrial automation initiatives. Europe Silicon Carbidemarket revenue growth is driven by Germany and France, due to significantly high demand for Silicon Carbide from automotive industry and rising focus on EVs, green technology, and decarbonization and renewable energy initiatives.

Silicon Carbide Market Competitive Landscape:

Company List:

- Wolfspeed, Inc. (formerly Cree)

- Infineon Technologies AG

- STMicroelectronics

- Onsemi

- ROHM Co., Ltd.

- Renesas Electronics Corporation

- Fuji Electric Co., Ltd.

- SK Siltron Co., Ltd.

- Entegris, Inc.

- Washington Mills

- Saint-Gobain

- CoorsTek

- Carborundum Universal Limited

- Grindwell Norton Ltd.

- Imerys

Competitive Landscape:

The competitive landscape in the Silicon Carbide market is intensifying, with major players adopting various strategies to account for larger market share. Technological innovation, strategic partnerships, and capacity expansion are key options as demand for SiC for applications in electric vehicles, power electronics, and renewable energy continues to grow. Leading companies are also focused on scaling production capabilities and enhancing product performance. Major companies such as Cree (Wolfspeed), Infineon Technologies AG, STMicroelectronics, Onsemi, and others are investing significantly in R&D to develop next-generation SiC products that offer superior efficiency and durability, catering to high-demand applications like fast-charging EV infrastructure and advanced telecommunications.

Also, many companies are establishing Joint Ventures (JVs) and strategic collaborations with automotive and energy companies, enabling them to integrate SiC solutions directly into EV and power systems. In addition, mergers and acquisitions are common as companies seek to expand their technical capabilities and geographical reach. Expanding wafer fabrication capacities, such as shifting to 6-inch or 8-inch wafers, also enables companies to meet the rising volume demands and achieve economies of scale, reducing production costs.

Companies are also focusing on sustainable practices, recognizing that energy efficiency is a critical selling point in green technology sectors. By adopting strategies that blend technical innovation, partnerships, and operational efficiency, leading SiC companies aim to strengthen their market position, meet diverse industry needs, and drive long-term growth amid the expanding demand for power-efficient, high-performance applications.

Recent Developments

- September 24, 2024: STMicroelectronics, which is a leading semiconductor provider in diverse electronics markets, unveiled its fourth-generation STPOWER Silicon Carbide(SiC) MOSFET technology. This latest generation establishes new standards in energy efficiency, power density, and durability. Designed to meet both automotive and industrial requirements, it is especially optimized for traction inverters, a crucial element in electric vehicle powertrains. ST aims to continue enhancing SiC technology through 2027, underscoring its commitment to innovation. As a leader in SiC power MOSFETs, ST seeks to capitalize on SiC’s superior efficiency and power density compared to traditional silicon technology. This advanced SiC generation supports future EV traction inverter designs, offering improvements in size reduction and energy savings. The 750V class of the fourth-generation platform has already been qualified, with the 1200V class set for completion by the first quarter of 2025. Commercial release of 750V and 1200V devices will follow, enabling engineers to target applications ranging from standard AC-line voltages to high-voltage EV batteries and charging systems.

- September 24, 2024: Resonac Corporation (formerly Showa Denko K.K.) and Soitec (Euronext Paris - Tech Leaders) announced a collaboration to develop 200mm (8-inch) SmartSiC Silicon Carbide(SiC) wafers. This partnership will leverage Resonac’s substrate and epitaxy expertise to advance Soitec’s high-efficiency SiC technology in both Japan and global markets. SmartSiC is an innovative semiconductor material offering significant performance advantages over traditional silicon in power-intensive applications, particularly for electric mobility and industrial sectors. By enabling more efficient power conversion, reduced system size and weight, and cost savings, SmartSiC is positioned to meet the increasing demands for efficient, compact, and economical solutions in automotive and industrial technologies.

- June 10, 2024: Mitsubishi introduced new 3.3kV/400A and 3.3kV/200A Silicon Carbide(SiC) MOSFET modules with embedded Schottky barrier diodes (SBDs). These modules, part of the Unifull series, are optimized for use in large industrial equipment such as rolling stock and power systems, joining the previously released 3.3kV/800A module. Designed to support the rising demand for high-performance inverters, these modules offer improved power output and conversion efficiency. Mitsubishi Electric also presented these at Power Conversion Intelligent Motion (PCIM) Europe 2024 in Nuremberg, Germany, from June 11 to 13.

Frequently Asked Questions:

Q: What is the global Silicon Carbidemarket size in 2024 and what is the projection for 2034?

A: The global Silicon Carbidemarket size was calculated at USD 4.21 billion in 2024 and expected to reach USD 12.56 billion in 2034

Which regional market accounted for largest revenue share in 2023, and what is the expected trend over the forecast period?

A: Asia Pacific is expected to account for largest revenue share in the global market over the forecast period.

Q: Which are the major companies are included in the global Silicon Carbidemarket report?

A: Major companies in the market report are Wolfspeed, Inc. (formerly Cree), Infineon Technologies AG, STMicroelectronics, Onsemi, ROHM Co., Ltd., Renesas Electronics Corporation, Fuji Electric Co., Ltd., SK Siltron Co., Ltd., Entegris, Inc., Washington Mills, Saint-Gobain, CoorsTek, Carborundum Universal Limited, Grindwell Norton Ltd., Imerys.

Q: What is the projected revenue CAGR of the global Silicon Carbidemarket over the forecast period?

A: The global Silicon Carbidemarket is expected to register a CAGR of 11.56% between 2025 and 2034.

Q: What are some key factors driving revenue growth of the Silicon Carbidemarket ?

A: Some key factors driving market revenue growth are rising demand from Electric Vehicles (EVs), advancements in power electronics, and expanding renewable energy industries, driven by high thermal conductivity, efficiency, and durability of SiC. Also, increasing use in solar and wind energy infrastructure to improve power conversion is expected to support revenue growth of the market to a major extent.

FAQ

Frequently Asked Question

What is the global demand for Silicon Carbide in terms of revenue?

-

The global Silicon Carbide valued at USD 4.21 Billion in 2024 and is expected to reach USD 12.56 Billion in 2034 growing at a CAGR of 11.56%.

Which are the prominent players in the market?

-

The prominent players in the market are Wolfspeed, Inc. (formerly Cree), Infineon Technologies AG, STMicroelectronics, Onsemi, ROHM Co., Ltd., Renesas Electronics Corporation, Fuji Electric Co., Ltd., SK Siltron Co., Ltd., Entegris, Inc., Washington Mills, Saint-Gobain, CoorsTek, Carborundum Universal Limited, Grindwell Norton Ltd., Imerys..

At what CAGR is the market projected to grow within the forecast period?

-

The market is project to grow at a CAGR of 11.56% between 2025 and 2034.

What are the driving factors fueling the growth of the market.

-

The driving factors of the Silicon Carbide include

Which region accounted for the largest share in the market?

-

Asia Pacific was the leading regional segment of the Silicon Carbide in 2024.