Knee Reconstruction Devices Market

Knee Reconstruction Devices Market - Global Industry Assessment & Forecast

230

2023

Dec - 2024

![]()

![]()

![]()

VMR-3806

Segments Covered

By

Product Cemented Implants, Cementless Implants, Partial Implants, Revision Implants

By

Product Cemented Implants, Cementless Implants, Partial Implants, Revision Implants

-

By

End User Hospitals, Orthopedic Clinics, ASCs

-

By

Indication Osteoarthritis, Rheumatoid Arthritis, Trauma, Others

-

By

Region North America, Europe, Asia Pacific, Latin America, Middle East and Africa

Snapshot

| 2023 | |

| 2024 - 2032 | |

| 2018 - 2022 | |

| USD 8.9 Billion | |

| USD 13.1 Billion | |

| 5.0% | |

| Europe | |

| North America |

Customization Offered

Cross-segment Market Size and

Analysis

for Mentioned Segments

Cross-segment Market Size and

Analysis

for Mentioned Segments- Additional Company Profiles (Upto 5

With

No Cost)

- Additional Countries (Apart From

Mentioned Countries)

- Country/Region-specific Report

- Go To Market Strategy

- Region Specific Market Dynamics

- Region Level Market Share

- Import Export Analysis

- Production Analysis

- Others Request

Customization Speak To

Analyst

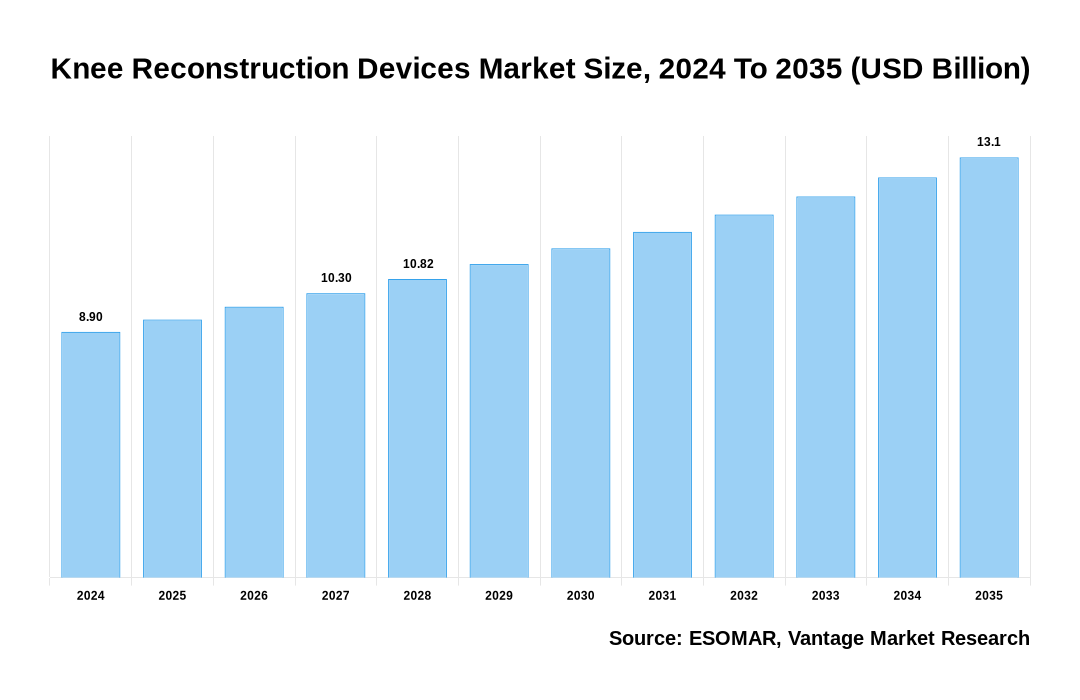

The global Knee Reconstruction Devices Market is valued at USD 8.9 Billion in 2024 and is projected to reach a value of USD 13.1 Billion by 2035 at a CAGR (Compound Annual Growth Rate) of 5.0% between 2025 and 2035. The Knee Reconstruction Devices market is driven by prevalence of arthritis, technological advancements, rising aging population and well-structured healthcare policies in many countries.

Key Highlights

- In 2024, based on the Product, the Cemented Implants category holds the largest market share in Knee Reconstruction Devices market

- Based on the Indication, the Osteoarthritis category holds the largest market share in 2024

- In 2024, based on the End User, the Hospitals category holds the largest market share

- North America dominated the Knee Reconstruction Devices market with largest market share of 42.4% in 2024

- Asia Pacific region is anticipated to grow at the highest CAGR during the forecast period

Knee Reconstruction Devices Market Size, 2023 To 2032 (USD Billion)

AI (GPT) is here !!! Ask questions about Knee Reconstruction Devices Market

Product Overview

The product segment is divided into cemented implants, cementless implants, partial implants, and revision implants. The cemented implants segment held the largest market share in 2024.

The cemented implants segment dominated the Knee Reconstruction Devices market because of its widespread adoption, due to their enhanced stability and immediate fixation capabilities, making them suitable for patients with weaker bone quality, such as those with osteoporosis. Additionally, their cost-effectiveness compared to cementless implants and a well-established track record in clinical outcomes have boost their preference among surgeons and patients alike. The segment is driven by the increasing prevalence of knee-related disorders, an aging population, and advancements in implant materials and designs that enhance longevity and patient comfort.

The partial implants segment is expected to experience robust growth of CAGR during the forecast period, driven by technological advancements in implant design and instrumentation, improved surgical techniques, and enhanced patient outcomes. The increasing emphasis on personalized medicine and the preference for preserving natural knee anatomy when feasible further boost the growth rate of the partial implants segment in the Knee Reconstruction Devices market.

End User Overview

The End User segment is divided into Hospitals, Orthopedic Clinics, and ASCs. The hospitals segment held the largest market share in 2024 for Knee Reconstruction Devices market.

The hospital segment is driven by the availability of advanced facilities and the continuous growth of healthcare infrastructure within hospitals. The hospital segment is expected to maintain its leading position in the upcoming years, fueled by an increasing number of orthopedic surgeries conducted in hospitals and a rising influx of patients seeking medical attention for orthopedic injuries.

The orthopedic clinics segment held a significant share of the Knee Reconstruction Devices market. The growing preference for outpatient procedures, advancements in minimally invasive techniques, and the availability of state-of-the-art equipment in these clinics have further boost their demand. Additionally, the personalized care and follow-up services provided by orthopedic clinics enhance patient satisfaction and outcomes, making them a preferred choice for knee reconstruction procedures.

Indication Overview

The indication segment is divided into Osteoarthritis, Rheumatoid Arthritis, Trauma, and others. The osteoarthritis segment held the largest market share in 2024.

Osteoarthritis is one of the significant contributors to years lived with disability among the musculoskeletal conditions. As osteoarthritis is more prevalent in older people (about 70% are older than 55), global prevalence is expected to increase with the ageing of population. The typical onset is in the late 40s to mid-50s, although osteoarthritis may also affect younger people, including athletes and people who sustain joint injury or trauma. About 60% of people living with osteoarthritis are women. According to World Health Organization, In 2019, about 528 million people worldwide were living with osteoarthritis; an increase of 113% since 1990. A prevalence of 365 million, the knee is the most frequently affected joint, followed by the hip and the hand.

Regional Overview

In 2024, the North America captured largest revenue share of 42.4%.

North America Knee Reconstruction Devices market is driven by high incidence of knee related conditions such as arthritis and gout, advancement in surgical technology and robotic navigation systems, as well as the presence of leading market players driving innovation in knee replacement and reconstruction. The growing awareness about knee conditions, higher privilege for minimally invasive surgeries, the availability of innovative and technologically advanced implant options and strategic collaborations and partnerships between healthcare providers and medical device manufacturers contribute to market growth and drive the growth of the North American market growth.

U.S. Knee Reconstruction Devices Market

The U.S. {Keyword}} market is driven by the rising prevalence of knee disorders such as osteoarthritis and rheumatoid arthritis, particularly among the aging population. The expanding patient pool and increased prevalence of lifestyle-related illnesses are also contributing to the knee reconstruction devices market's expansion. In U.S. number of companies producing knee reconstructive devices continues to grow, competition in the industry is heating up.

Europe Knee Reconstruction Devices Market

The European Knee Reconstruction Devices market is expected to account for a substantial share driven by expanding aging population and the increasing prevalence of arthritis across the region. Additionally, the market benefits from a rising number of individuals affected by chronic diseases and improving affordability of knee implants, which make these devices more accessible. These factors collectively position Europe as a key region for market expansion in the years ahead. For Instance, In October 2024, Smith+Nephew is the global medical technology company announced today that its LEGION Hinged Knee (HK) System is now available in the United States with proprietary OXINIUM (Oxidized Zirconium) implant technology that delivers the durability of metals, the wear resistance of ceramics, and corrosion resistance better than both.

Key Trends

- Rising Prevalence of Knee Disorders: Increasing cases of osteoarthritis, rheumatoid arthritis, and sports injuries are driving the demand for knee reconstruction devices globally

- Aging Population: The growing elderly population is contributing to a higher incidence of knee-related conditions, boosting the Knee Reconstruction Devices market

- Technological Advancements: Innovations such as 3D-printed implants, robotics-assisted surgeries, and patient-specific knee implants are transforming the Knee Reconstruction Devices market

- Minimally Invasive Procedures: Surgeons and patients are increasingly opting for less invasive techniques, leading to faster recovery times and reduced hospital stays

- Shift Towards Cementless Implants: Growing preference for cementless implants due to their long-term benefits and suitability for younger, more active patients

- Focus on Post-Surgery Rehabilitation: Companies are integrating digital technologies like mobile apps and wearables to improve post-operative care and patient compliance

Report Coverage & Deliverables

Get Access Now

Track market trends LIVE & outsmart rivals with our Premium Data Intel Tool: Vantage Point

Market Dynamics

The growing aging population suffering from knee-relevant disorders such as arthritis and osteoarthritis drives the Knee Reconstruction Devices market

By 2030, 1 in 6 people in the world will be aged 60 years or over. At this time the share of the population aged 60 years and over will increase from 1 billion in 2020 to 1.4 billion. By 2050, the world’s population of people aged 60 years and older will double (2.1 billion). The number of persons aged 80 years or older is expected to triple between 2020 and 2050 to reach 426 million. As per the same source, around 32.5 million adults from the United States have osteoarthritis. In addition, factors such as the growing adoption of technological developments and favorable reimbursement policies propel the Knee Reconstruction Devices market growth. Many countries worldwide have become medical tourism points for knee reconstruction surgeries, as they provide quality treatment at affordable prices. Total joint replacement of a dysfunctional knee using artificial knee implants has been a reliable and efficient treatment method.

Technological Advancement

The increasing number of advancements in surgical techniques and implant materials, rapid adoption of minimally invasive surgeries, rising demand for personalized and patient-specific knee implants and technological advancements in knee reconstruction devices drives the growth rate of the Knee Reconstruction Devices market. Favorable compensation policies for knee reconstruction procedures, growing awareness about the benefits of knee reconstruction surgeries, increasing participation in sports and recreational activities leading to knee injuries and the growing number of strategic collaborations and partnerships between medical device manufacturers and healthcare providers further promote the Knee Reconstruction Devices market growth.

Competitive Landscape

The Knee Reconstruction Devices market is characterized by the presence of both established players and emerging companies, each strive for market share through product innovation, strategic partnerships, and geographic expansion. Industry giants like Aesculap Inc, Zimmer Biomet, MicorPort Scientific, DePuy Synthes, Medacta, Stryker Corporation, Smith & Nephew, Tornier Inc., Exactech Inc. Organizations operating within this sector prioritize technological advancements, strategic alliances, and user experience improvement. These key players are expected to maintain their leadership in the knee arthroplasty sector and achieve substantial revenue growth in the years to come.

The key players in the global Knee Reconstruction Devices market include - Aesculap Inc, Zimmer Biomet, MicorPort Scientific, DePuy Synthes, Medacta, Stryker Corporation, Smith & Nephew, Tornier Inc., Exactech Inc. among others.

Recent Market Developments

Zimmer Biomet Receives FDA Approval for Oxford® Cementless Partial Knee, Only Cementless Partial Knee Replacement Implant in the U.S.

- In November 2024, Zimmer Biomet Holdings, Inc. is a global medical technology leader, today announced U.S. Food and Drug Administration (FDA) Premarket Approval Application (PMA) Supplement approval for the Oxford® Cementless Partial Knee. The approval is based on safety and effectiveness data from an Investigational Device Exemption (IDE) study and non-clinical testing for cementless partial knee replacement (PKR).1 The Oxford Cementless Partial Knee allows surgeons to perform a PKR with improved fixation,2 better long-term implant survival rate2,3 and improved efficiency in the operating room4 (OR) compared to the Oxford Cemented Partial Knee procedure

Next advancement of Mako SmartRobotics™ delivers on its clinical history and technology as total Mako procedures surpass 1 million worldwide

- In 08 March 2023, Stryker Corporation is launch of Mako Total Knee 2.0, the next chapter in Mako SmartRobotics™, at the AAOS 2023 Annual Meeting in Las Vegas. Informed by over 500,000 Mako Total Knee procedures, Mako Total Knee 2.0 is designed to deliver the same, trusted outcomes surgeons expect from Mako with a new, elevated user experience

Smith+Nephew introduces first of its kind handheld digital tensioning device for robotically-enabled total knee arthroplasty

- In April 2023, Smith+Nephew is the global medical technology company, today introduced its new CORI◊ Digital Tensioner - a purpose built device that lets surgeons measure the ligament tension in a knee prior to cutting bone. By enabling a surgeon to quantify joint laxity in the native knee and achieve an optimal ligament tensioning force, the CORI Digital Tensioner helps to reduce variability when balancing the knee in surgery. This helps make surgical planning more objective versus other commercially available alternatives

The global Knee Reconstruction Devices market can be categorized as Product, Indication, End Use and Region.

| Parameter | Details |

|---|---|

| Segments Covered |

By Product

By End User

By Indication

By Region

|

| Regions & Countries Covered |

|

| Companies Covered |

|

| Report Coverage | Market growth drivers, restraints, opportunities, Porter’s five forces analysis, PEST analysis, value chain analysis, regulatory landscape, technology landscape, patent analysis, market attractiveness analysis by segments and North America, company market share analysis, and COVID-19 impact analysis |

| Pricing and purchase options | Avail of customized purchase options to meet your exact research needs. Explore purchase options |

FAQ

Frequently Asked Question

What is the global demand for Knee Reconstruction Devices in terms of revenue?

-

The global Knee Reconstruction Devices valued at USD 8.9 Billion in 2023 and is expected to reach USD 13.1 Billion in 2032 growing at a CAGR of 5.0%.

Which are the prominent players in the market?

-

The prominent players in the market are Aesculap Inc, Zimmer Biomet, MicorPort Scientific, DePuy Synthes, Medacta, Stryker Corporation, Smith & Nephew, Tornier Inc., Exactech Inc..

At what CAGR is the market projected to grow within the forecast period?

-

The market is project to grow at a CAGR of 5.0% between 2024 and 2032.

What are the driving factors fueling the growth of the market.

-

The driving factors of the Knee Reconstruction Devices include

Which region accounted for the largest share in the market?

-

North America was the leading regional segment of the Knee Reconstruction Devices in 2023.