EV Battery Recycling Market

EV Battery Recycling Market - Global Industry Assessment & Forecast

210

2023

Aug - 2024

![]()

![]()

![]()

VMR-2579

Segments Covered

By

Chemistry Lithium-ion Battery, Lead-acid, Nickel, Others

By

Chemistry Lithium-ion Battery, Lead-acid, Nickel, Others

-

By

Process Pyrometallurgical, Hydrometallurgical, Others

-

By

Vehicle Type Passenger Cars, Buses, Vans, Others

-

By

End User Transportation, Consumer electronics, Industrial

-

By

Region North America , Europe , Asia Pacific , Latin America , The Middle-East and Africa

Snapshot

| 2023 | |

| 2024 - 2032 | |

| 2018 - 2022 | |

| USD 1.21 Billion | |

| USD 12.67 Billion | |

| 29.82 % | |

| Asia Pacific | |

| Asia Pacific |

Customization Offered

Cross-segment Market Size and

Analysis

for Mentioned Segments

Cross-segment Market Size and

Analysis

for Mentioned Segments- Additional Company Profiles (Upto 5

With

No Cost)

- Additional Countries (Apart From

Mentioned Countries)

- Country/Region-specific Report

- Go To Market Strategy

- Region Specific Market Dynamics

- Region Level Market Share

- Import Export Analysis

- Production Analysis

- Others Request

Customization Speak To

Analyst

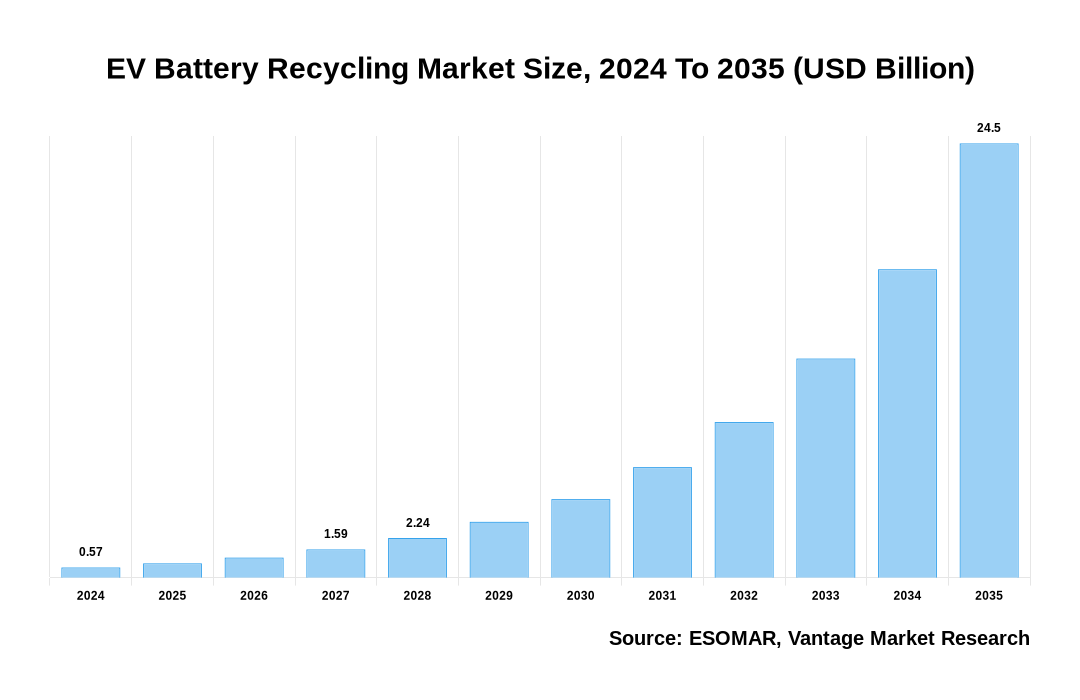

The global EV Battery Recycling Market is valued at USD 1.21 Billion in 2023 and is projected to reach a value of USD 12.67 Billion by 2032 at a CAGR (Compound Annual Growth Rate) of 29.82 % between 2024 and 2032.

Key Highlights

- In 2023, North America led the market with the highest revenue share of 53.1%

- Asia Pacific is expected to witness maximum market growth during the forecast period

- Policymakers globally are introducing regulations driven by concerns about carbon emissions, material shortages, and supply chain issues

- Based on chemistry, the Lithium-ion Battery segment dominated the market with the largest share globally from 2023 to 2030

- On the basis of the Vehicle Type, the Passenger Cars category accounted for about 77.1% of the market share in 2023

- Consumers' growing interest in electric vehicles (EVs) and the increasing sales are expected to generate a substantial number of end-of-life EV batteries (EVBs), driving the demand for battery recycling

EV Battery Recycling Market Size, 2023 To 2032 (USD Billion)

AI (GPT) is here !!! Ask questions about EV Battery Recycling Market

Regional Overview

North America Dominated Sales with a 53.1% share in 2023. This dominance is due to the significant growth in electric vehicle adoption and the presence of leading battery manufacturers in the region. Government initiatives in APAC countries aim to control pollution and promote EV use, driving market growth. Policies to reduce EV battery waste, concerns over precious metal depletion, and the rising demand for lithium-ion batteries further support this trend. Additionally, the increasing volume of battery waste and the high adoption of electric mobility contribute to the region's market leadership. Meanwhile, the Middle East & Africa is expected to register the highest CAGR during the forecast period.

India is the fastest-growing market in the Asia Pacific region and is further expected to expand the recycling capabilities from 2 GWh in 2023 to 128 GWh by 2030, according to Niti Aayog. This growth is driven by a 200% year-on-year increase in EV sales since the pandemic. However, India needs specialist policies and infrastructure to achieve its recycling targets due to the complexity of modern batteries. Currently, 90% of used batteries are processed by the unorganized sector or in landfills. Despite this, policies like FAME and FAME II promote EV adoption, and manufacturers like Tata AutoComp invest in R&D to provide affordable electric cars and solutions to extend the EV range.

China decommissioned about 200,000 metric tons (25 GWh) of NEV batteries by the end of 2020, a significant rise from 3 GWh in 2017. By 2025, battery replacement is expected to peak at 780,000 tons (116 GWh). The country follows a second-life strategy for NEV batteries, involving cascade utilization for batteries with 60-80% residual capacity and resource recycling. China, holding 77% of Asia's capacity, saw NEV numbers reach 5.51 million in March 2023, with 2021 sales at 3.3 million units. The recycling industry is growing at 78.4% annually, with over 15,000 companies involved. Local governments are also promoting recycling, with initiatives in Jiangsu and Shanghai.

Japan pioneered e-waste recycling by enacting the Basic Act on Establishing a Sound Material-Cycle Society in 2000. This law promotes effective resource utilization, allowing companies flexibility in managing collection schemes. Auto manufacturers have partnered with logistics and metal refining companies to establish a value chain for recycling. Japan's approach to battery recycling is liberal, encouraging voluntary collection and recycling through the 1991 act. This ordinance sets mandatory recycling material ratios for various batteries. The Japan Battery Recycling Centre (JBRC) has established a specific supply chain mechanism for small portable batteries. Companies collaborate to adjust recycling technology and manage the value chain based on their capacity and changing economic conditions.

The Inflation Reduction Act incentivizes buying and selling new electric vehicles (EVs) with a federal tax credit of up to USD 7,500. By 2027, 80% of EV battery minerals must be sourced from North America or U.S. free-trade agreement countries. By 2029, 100% of battery components must be North American. From 2024, EVs with Chinese battery components will not qualify for the Clean Vehicle Credit. The Department of Energy (DOE) announced USD 37 million to reduce battery recycling costs, aiming for EVs to be half of all new light-duty vehicle sales by 2030. A study by Ascend Elements shows increasing concern about EV battery disposal despite the booming recycling industry. Regulatory incentives, like the Inflation Reduction Act, offer significant tax credits for recycled battery materials, even if not initially mined in the U.S. or free-trade countries.

By 2030, around 1.2 million EV batteries will reach their end-of-life, increasing significantly to 2.6 million by 2035 and 5.4 million by 2040. The recycling industry needs to be developed, and advanced infrastructure is required to handle future volumes. A clear, stable regulatory framework in the EU will encourage long-term investments in recycling infrastructure. Developing a lithium-ion battery recycling sector could attract broader investment for manufacturing facilities. Although the EU leads in lead-acid batteries, its capacity for lithium-ion cells is small, with most imports coming from China. Leveraging EU strengths in battery technology R&D and forming synergies with existing manufacturing can scale up traction battery production, supported by foreign investment (European Commission, 2016).

Value Chain Analysis Overview

The value chain involves four key steps:

- Collecting, transporting, and sorting batteries

- Discharging and dismantling them

- Shredding and producing black mass

- Recovering materials using chemical processes

The final step, critical for closing the circularity loop, involves refining materials through pyrometallurgy or hydrometallurgy to produce battery-grade content. While pyrometallurgy is more robust, it recovers fewer materials. The materials recovery stage offers the highest profit potential due to high-value recycled materials but has significant entry barriers due to high capital requirements and expertise needed. Earlier steps in the value chain are less profitable but more manageable to enter, with lower risks and required skills. However, overcapacity in shredding due to scrap shortages reduces margins, making the materials recovery stage more attractive for ambitious players. Traditional recyclers should aim for a share of the materials recovery profits rather than just the initial stages.

Key Trends

- Rising environmental concerns and favourable government policies are driving the demand for EVs, which are projected to reach over 5 million annual sales by 2025. This surge is boosting the market growth, as more EVs on the road means a greater need for battery recycling.

- Major companies are making substantial investments in electric vehicles, a clear indication of the business potential in the EV industry. For instance, Amazon is planning to invest nearly USD 975 million in electric vans, trucks, and low-emission hubs in Europe by 2027. This significant investment is not only promoting sustainable logistics but also driving the demand for efficient solutions.

- Government initiatives are playing a pivotal role in accelerating the adoption of EVs. Worldwide, policies are being implemented to curb the use of internal combustion engine vehicles. For instance, Britain and France have set a target to ban gasoline and diesel car sales by 2040. In India, the Electric Mobility Promotion Scheme 2024, with a budget of Rs. 500 crores, is specifically designed to boost EV adoption. These policies are not only driving the growth of the market but also shaping the future of the EV industry.

- Companies are investing in advanced recycling technologies to reduce costs and improve efficiency. Developments like direct cathode recycling and the establishment of new recycling plants are notable. For instance, BatX Energies raised USD 5 million to scale production and establish a nationwide reverse logistics network. Additionally, Tata Chemicals and Ziotrax Cleantech Pvt Ltd. are setting up recycling operations to recover valuable materials from used batteries, reduce environmental pollution, and conserve resources.

Regulatory Scenario

Policymakers globally are introducing regulations to support EV Battery Recycling, driven by concerns about carbon emissions, material shortages, and supply chain issues. The EU's Battery Regulation, adopted in July 2023, covers the entire battery life cycle. It mandates a Battery Passport for EV and industrial batteries over 2 kWh by February 2027 and sets recycling targets of 50% for lithium, 90% for cobalt, and 90% for nickel by the end of 2027. Targets for recycled materials in new batteries are also set, with percentages increasing by 2031 and 2036.

The EU's Critical Raw Materials Act aims for 25% of annual demand for critical materials from recycling. In China, regulations since 2018 require EV manufacturers to establish recycling systems with high recovery targets for cobalt, nickel, and lithium. The US lacks specific recycling regulations but promotes domestic sourcing and supports battery recycling projects through the Inflation Reduction Act and other initiatives.

Report Coverage & Deliverables

Get Access Now

Track market trends LIVE & outsmart rivals with our Premium Data Intel Tool: Vantage Point

Market Dynamics

Increasing consumer interest in EVs, rising EV sales, and expanding battery recycling capacity

Consumers' growing interest in electric vehicles (EVs) and the increasing sales are expected to generate a substantial number of end-of-life EV batteries (EVBs), driving the demand for battery recycling. EVB recycling companies are anticipated to scale up their recycling capabilities to accommodate the growing volume of batteries from both new sales and second-life sources, fueling market growth throughout the forecast period. Innovations in recycling processes, such as Ascend Elements and Koura's Hydro-to-Anode technique, which recovers high-purity graphite from spent batteries, also contribute to market expansion. This innovative approach facilitates cost-effective lithium-ion (Li-ion) battery recycling and reduces the need for new material mining.

High operational costs, logistical challenges, and uncertainties in battery refurbishment

Despite growth opportunities, the EV Battery Recycling market faces challenges. Operating costs, including transportation and collection expenses at recycling plants, are significantly higher. The complex extraction processes involved in retrieving battery components and uncertainties regarding the safety, efficiency, and remaining lifespan of refurbished batteries pose additional hurdles. These factors could impede the widespread adoption of large-scale second-life battery applications and overall industry development.

Advancements in battery testing, eco-friendly battery adoption, and supply chain expansion present several growth opportunities

The EV Battery Recycling market presents several growth opportunities. Advancements in testing methodologies for alternative cathode materials and efficient recycling systems enhance the industry's capabilities. The increasing adoption of eco-friendly batteries and the expansion of the battery supply chain offer additional avenues for market expansion. Moreover, the recovery of economies in developing nations and the global shift towards sustainable practices further support the flourishing of the EV Battery Recycling market.

Competitive Landscape

The EV Battery Recycling market is highly competitive, driven by companies expanding through collaborations and partnerships. In January 2023, Lohum partnered with Mercedes Benz to recycle used batteries from e-rickshaws in India. EV manufacturers are also shifting towards eco-friendly materials; Ford uses bio-based and recycled materials for vehicle exteriors, while Nissan uses old car parts, water bottles, plastic bags, and home appliances for interiors and exteriors. Companies are heavily investing in recycling facilities and increasing the use of recycled raw materials in their manufacturing processes.

Recent Market Developments

Honda Motor and Mitsubishi Corp. - Altna Joint Venture Collaboration

- In June 2024, Honda Motor and Mitsubishi Corp. will establish a new company in July that will give a second life to used electric vehicle batteries in Japan, thus reducing the cost of driving an EV. The joint venture, Altna, aims to develop new services in anticipation of the broader use of EVs.

Omega Seiki Private Ltd (OSPL) and Attero Collaboration

- In February 2024, Omega Seiki Private Ltd (OSPL) made a significant move towards a more sustainable future by signing an agreement with Attero to recycle lithium-ion batteries. With plans to recycle over 100MWh of batteries in the next 3-4 years, this strategic alliance will substantially impact the domestic market, ASEAN, and African regions, contributing to a more sustainable future.

BASF and Stena Recycling Collaboration

- In January 2024, BASF and Stena Recycling finalized a black mass purchase agreement as part of their more extensive collaboration to establish a battery recycling value chain for the European EV battery market. BASF is a global producer and recycler of battery materials.

Renault's Closed-Loop Recycling Initiative

- In March 2024, Renault is pioneering a groundbreaking initiative to develop a closed-loop recycling process for EV batteries in Europe. The project aims to significantly diminish Europe's reliance on imported battery materials, particularly from China. The French automaker's project could stimulate billions in revenue and contribute to a more sustainable automotive sector.

The global EV Battery Recycling market can be categorized as Chemistry, Process, Application, and Region.

| Parameter | Details |

|---|---|

| Segments Covered |

By Chemistry

By Process

By Vehicle Type

By End User

By Region

|

| Regions & Countries Covered |

|

| Companies Covered |

|

| Report Coverage | Market growth drivers, restraints, opportunities, Porter’s five forces analysis, PEST analysis, value chain analysis, regulatory landscape, technology landscape, patent analysis, market attractiveness analysis by segments and North America, company market share analysis, and COVID-19 impact analysis |

| Pricing and purchase options | Avail of customized purchase options to meet your exact research needs. Explore purchase options |

FAQ

Frequently Asked Question

What is the global demand for EV Battery Recycling in terms of revenue?

-

The global EV Battery Recycling valued at USD 1.21 Billion in 2023 and is expected to reach USD 12.67 Billion in 2032 growing at a CAGR of 29.82 %.

Which are the prominent players in the market?

-

The prominent players in the market are ACCUREC Recycling GmbH, Battery Solutions LLC, Gopher Resource LLC, Ecobat Logistics, Terrapure BR Ltd., East Penn Manufacturing Company, Retriev Technologies, COM2 Recycling Solutions, Call2Recycle, Exide Technologies, Gravita India Ltd., Snam S.p.A., Umicore N.V..

At what CAGR is the market projected to grow within the forecast period?

-

The market is project to grow at a CAGR of 29.82 % between 2024 and 2032.

What are the driving factors fueling the growth of the market.

-

The driving factors of the EV Battery Recycling include

Which region accounted for the largest share in the market?

-

Asia Pacific was the leading regional segment of the EV Battery Recycling in 2023.