Data Center Colocation Market

Data Center Colocation Market - Global Industry Assessment & Forecast

148

2022

Feb - 2023

![]()

![]()

![]()

VMR-2012

Segments Covered

By

Types Retail Colocation, Wholesale Colocation

By

Types Retail Colocation, Wholesale Colocation

-

By

End Users Small & Medium-Sized Enterprises (SMEs), Large Enterprises

-

By

Industry Banking Financial Services, & Insurance (BFSI), IT & Telecom, Government & Defense, Healthcare, Research & Academics, Retail, Energy, Manufacturing, Other Industries (Media, Entertainment, Transportation & Logistics)

-

By

Region North America, Europe, Asia Pacific, Latin America, Middle East & Africa

Snapshot

| 2022 | |

| 2023 - 2030 | |

| 2017 - 2021 | |

| USD 56.45 Billion | |

| USD 149.02 Billion | |

| 12.90% | |

| Asia Pacific | |

| North America |

Customization Offered

Cross-segment Market Size and

Analysis

for Mentioned Segments

Cross-segment Market Size and

Analysis

for Mentioned Segments- Additional Company Profiles (Upto 5

With

No Cost)

- Additional Countries (Apart From

Mentioned Countries)

- Country/Region-specific Report

- Go To Market Strategy

- Region Specific Market Dynamics

- Region Level Market Share

- Import Export Analysis

- Production Analysis

- Others Request

Customization Speak To

Analyst

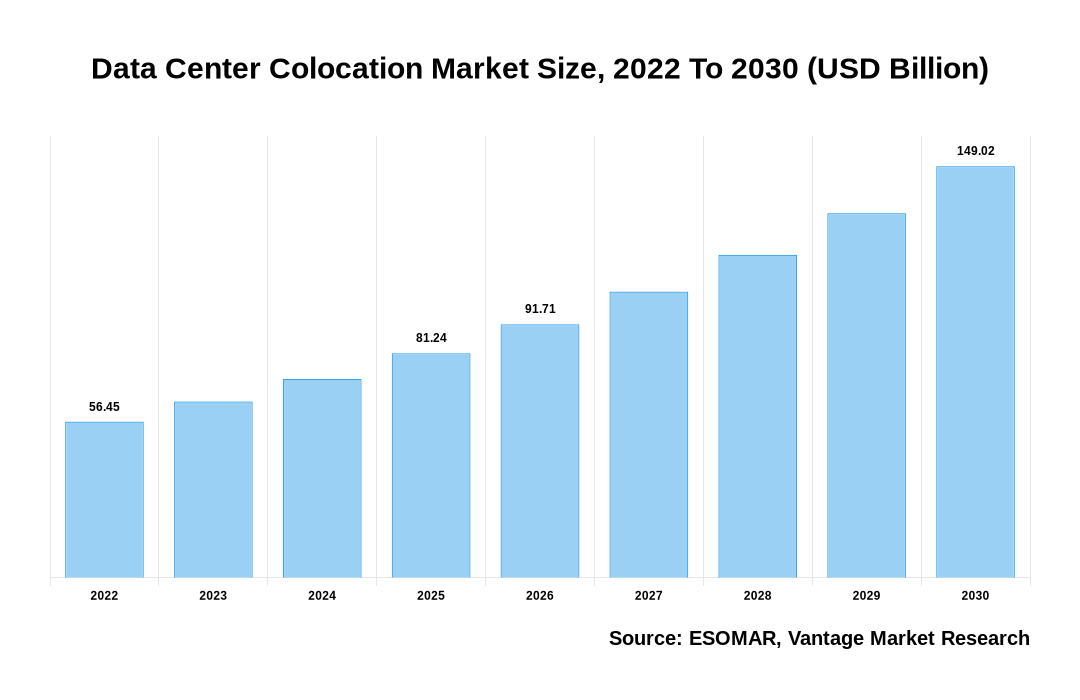

The Global Data Center Colocation Market is valued at USD 56.45 Billion in 2022 and is projected to reach USD 149.02 Billion by 2030 at a CAGR of 12.90% over the forecast period.

Premium Insights

Data centers have developed as an indispensable component of current business processes, hosting important corporate applications. IT infrastructure has evolved into a requirement for firms seeking to run their operations efficiently. As the need for data centers has increased in recent years, cloud and colocation have become valuable assets for many firms looking to expand their IT capabilities. Colocation data centers were a blessing for organizations that wanted rapid IT upscaling but lacked the necessary skills and financial resources.

Data Center Colocation Market Size, 2022 To 2030 (USD Billion)

AI (GPT) is here !!! Ask questions about Data Center Colocation Market

The rising requirement for scalable data centers, which has reduced total IT investment, and the increasing complexity of data centers are the market's primary growth factors. The industry is also rising due to the increased use of automation and robots in server installation, disc storage management, and connection management. As a result, the high expenses of owning and operating a data center, particularly for organizations that generate uneven data quantities, are projected to support industry expansion.

Aside from cost reductions, Data Center Colocation provides various additional advantages to consumers. According to research, owning or developing a data center facility can cost more than USD 300 per square foot, not including laying the necessary fiber cable. In such cases, handling a whole data center facility in-house is a high-cost component for SMEs, but large-scale enterprises may easily tolerate this expense. Data Center Colocation is such a solution that provides SMEs with a feasible and cost-effective option for renting data center space, which is projected to fuel market expansion during the forecast period.

Report Coverage & Deliverables

- Real-Time Data Updates:

- Competitor Benchmarking

- Market Trends Heatmap

- Custom Research Queries

- Market Sentiment Analysis

- Demographic and Geographic Insights

Get Access Now

Furthermore, the continuous use of novel technologies, such as cloud computing, the internet of things (IoT), autonomous cars, and sophisticated robotics, is growing demand for Data Center Colocation. The continued advancement of these technologies has also resulted in the widespread deployment of intelligent gadgets, necessitating decreased latency.

As a result, cloud service providers may relocate their data center facilities closer to their consumers, providing high bandwidth and low latency in data transfer. Furthermore, the growing demand for lower latency in data transfers and enhanced connection, as well as the increasing penetration of smart devices, is expected to drive demand for colocation data centers. On the other side, the market potential is limited when there is an inability to create a server farm close to the specific organization. Many firms need more motivation to accept and implement server farms. The cause of this anxiety is an over-reliance on workers and allowing them to overpower them completely. Over time, each of these elements will limit the expansion of the Data Center Colocation industry.

Top Market Trends

1. Increasing demand for public cloud and IoT: Large businesses increasingly use cloud computing technology to improve operations and assure scalability. Because of this, they are more inclined to choose colocation services, which provide secure data storage and networking while also maintaining efficiency.

2. Growing penetration of social media and OTT platforms: The need for data centers and colocation services has increased due to the increasing volume of data from social media and over-the-top (OTT) platforms. Social media users are becoming increasingly engaged, helping to increase the amount of data available from these platforms.

3. Increasing penetration of advanced technologies: The growth of immersive technologies like augmented reality, virtual reality, and artificial intelligence (AI), as well as 5G technology, has further contributed to the requirement for providing larger bandwidths for data transfer across organizations. The continuous use of several disruptive technologies, including cloud computing, IoT, autonomous cars, and sophisticated robotics, is another factor driving the growing demand for colocation in data centers.

4. Reduction in the cost of IT infrastructure: To facilitate establishing a server farm on-site, talented IT professionals must do the responsibilities. Without a doubt, enabling also involves a variety of consumptions for supporting the board and the framework. Additionally, opening a new server farm office necessitates a significant initial investment and raises the enterprises' overall capital expenditures.

Market Segmentation

The Data Center Colocation Market is segmented based on the segmentation categories- Types, End User, Industry, and Region. Based on Types, the market is segmented into Retail Colocation and Wholesale Colocation. Furthermore, based on the End Users, the market is segmented into Small & Medium-Sized Enterprises (SMEs) and Large Enterprises. In addition, based on Industry, the market is segmented into Banking Financial Services & Insurance (BFSI), IT & Telecom, Government & Defense, Healthcare, Research & Academics, Retail, Energy, Manufacturing, and Other Industries (Media, Entertainment, Transportation & Logistics). In addition, based on Region, the market is segmented into North America, Europe, Asia Pacific, Latin America, and Middle East & Africa.

Based on Types

Retail Colocation Is Prime Revenue Contributor in the Market as It Provides Flexibility for Managing Huge Amounts of Data

Retail colocation dominated the market with the highest revenue share in 2021 and is estimated to sustain its dominance throughout the forecast period. Retail colocation allows businesses to rent a portion of a data center's space. This provides organizations with flexibility when managing tiny amounts of data or when infrastructure is only required for a brief time. It is especially helpful for small-scale enterprises with fewer data storage requirements than large organizations. Furthermore, the retail version is ideal for businesses who wish to take advantage of the benefits of colocation services but have a restricted budget. Conversely, wholesale colocation is expected to register the highest CAGR over the forecast period because of the shift toward wholesale colocation by major cloud service providers and hyper scalers. Large organizations have a massive client base, which results in the creation of vast amounts of data and the requirement for large commercial space to house their servers, creating a need for wholesale colocation.

Based on the End User

The Large Enterprises Accounted for The Highest Revenue Share in the Market Due to Rising Demand from Diversified Industries

The Large Enterprises segment dominated the market in 2021-22. This significant share is due to the high product demand among major enterprises to handle efficiently and store data. Large organizations from diverse industries worldwide create massive amounts of data, necessitating infrastructure with large storage capabilities. Data Center Colocation allows major organizations to lease substantial floor space close to consumers while also scaling up infrastructure based on demand from that specific region. In addition, the SME segment is predicted to record the highest CAGR over the forecast period due to the growing number of SMEs and start-ups in emerging countries such as China and India. Because SMEs have budgetary constraints, cost reduction becomes an important aspect of the organization's growth. Furthermore, using colocation data centers allows small businesses to save money on operating and fixed expenditures. As a result, SMEs choose to use colocation data center facilities rather than owning and maintaining them, fueling sector development.

Based on Industry

IT & Telecom Category Dominated the Market with Largest Share in the Market Due to Growing Internet Penetration Among the Consumers

The IT & telecom category held the largest share of the market in 2021. A significant proportion of this category is linked to the growing number of mobile internet users and the industry's ongoing development of new applications and software. According to the GSM Association (GSMA), around 4.5 billion people were connected to the mobile internet in 2020, an increase of 250 million users from 2020. This figure is expected to climb as phones with sophisticated functions become more popular. Meanwhile, the introduction of 5G is predicted to stimulate the expansion of the IT and telecom sectors, resulting in enormous data volumes and boosting market growth.

The healthcare segment is predicted to grow at a higher CAGR throughout the projected period because of the rising technological improvements in the hospital business. Furthermore, certain government rules, such as the American Recovery and Reinvestment Act of 2014, have made it mandatory for public and commercial healthcare service providers in the United States to keep patient Electronic Health Records (EHRs). As a result, healthcare practitioners need data storage solutions. The increasing volume of patient data collected worldwide is expected to boost product adoption in the healthcare sector. Furthermore, the worldwide pandemic will raise the demand for data storage in the healthcare industry for research purposes. As a result, it will drive segment growth over the forecast period.

Based on Region

North America is the Largest Revenue Contributor Due to the Presence of Major Industry Players

North America dominated the market and accounted for 43.6% market share of the global revenue in 2021 due to the strong presence of numerous large cloud service providers and SMEs establishing colocation data centers across the area. Furthermore, rising e-commerce sales in the United States boost the regional market growth. Retailers are extensively investing in their IT infrastructure to save consumer data that can be used to determine customer buying habits and product requests based on numerous categories such as area, gender, and age group. Since the pandemic breakout, the growing use of OTT platforms, streaming, and gaming has contributed to rising demand across North America. To accommodate the growing volume of data, various cloud service providers and social media businesses made significant investments in leasing colocation facilities in 2021. During 2021, overall inventory in the primary US market increased by 17% to 3,358 MW in capacity. With impending breakthroughs in 5G and IoT technologies, North America's Data Center Colocation market is likely to increase further in the next years.

Conversely, Asia Pacific is expected to grow at a higher CAGR throughout the projected period because of the region's growing internet users. The presence of some of the region's top IT BPO outsourcing service providers and software enterprises is also helping with industry growth. Furthermore, the increasing usage of smart products and technologies has resulted in greater data volumes, prompting enterprises across industries to establish data centers.

Competitive Landscape

The global Data Center Colocation market is dominated by companies such as China Telecom Corporation Limited, Coresite Realty Corporation, and Cyrusone Inc. because of their unique products, financial stability, strategic advances, and global reach. The participants are focusing their efforts on promoting R&D. Additionally; they support strategic expansion activities, including product launches, joint ventures, and partnerships to expand their client base and boost their market position. Some of the key players in the Global Data Center Colocation Market include- China Telecom Corporation Limited (China), Coresite Realty Corporation (US), Cyrusone Inc. (US), Cyxtera Technologies Inc. (US), Digital Realty Trust Inc. (US), Equinix Inc. (US), Global Switch (UK), KDDI Corporation (Japan), NTT Communications Corporation (Japan), Verizon Enterprise Solutions Inc. (US), to note a few.

Recent Market Developments

● In April 2022, Compass Datacenters, an American colocation company, developed a new business unit named Compass Quantum, which will provide modular data centres as a service. Each module provides enough space, power, and cooling to power 100kW of IT equipment in a 2N redundant arrangement.

● In March 2021, Digital Realty Trust, Inc. announced the acquisition of InterXion to fulfill the growing need for colocation and hyper-scale infrastructure in the Americas, Europe, and Asia Pacific. This acquisition has expanded the customer base as well as the product portfolio of the company.

Segmentation of the Global Data Center Colocation Market

Parameter

Details

Segments Covered

By Types

By End Users

By Industry

By Region

Regions & Countries Covered

Companies Covered

Report Coverage

Market growth drivers, restraints, opportunities, Porter’s five forces analysis, PEST

analysis, value chain analysis, regulatory landscape, technology landscape, patent analysis, market

attractiveness analysis by segments and North America, company market share analysis, and COVID-19

impact analysis

Pricing and purchase options

Avail of customized purchase options to meet your exact research needs. Explore purchase options

FAQ

Frequently Asked Question

What is the global demand for Data Center Colocation in terms of revenue?

-

The global Data Center Colocation valued at USD 56.45 Billion in 2022 and is expected to reach USD 149.02 Billion in 2030 growing at a CAGR of 12.90%.

Which are the prominent players in the market?

-

The prominent players in the market are China Telecom Corporation Limited (China), Coresite Realty Corporation (US), Cyrusone Inc. (US), Cyxtera Technologies Inc. (US), Digital Realty Trust Inc. (US), Equinix Inc. (US), Global Switch (UK), KDDI Corporation (Japan), NTT Communications Corporation (Japan), Verizon Enterprise Solutions Inc. (US).

At what CAGR is the market projected to grow within the forecast period?

-

The market is project to grow at a CAGR of 12.90% between 2023 and 2030.

What are the driving factors fueling the growth of the market.

-

The driving factors of the Data Center Colocation include

- Cost affordable IT operations

Which region accounted for the largest share in the market?

-

North America was the leading regional segment of the Data Center Colocation in 2022.