Chemical Vapor Deposition Market

Chemical Vapor Deposition Market - Global Industry Assessment & Forecast

240

2023

Sep - 2024

![]()

![]()

![]()

VMR-2638

Segments Covered

By

Category CVD Equipment, CVD Materials, CVD Services

By

Category CVD Equipment, CVD Materials, CVD Services

-

By

Application Semiconductor & Microelectronics, Data Storage, Solar Products, Cutting Tools, Medical Equipment, Others

-

By

Region North America, Europe, Asia Pacific, Latin America, Middle East & Africa

Snapshot

| 2023 | |

| 2024 - 2032 | |

| 2018 - 2022 | |

| USD 22.91 Billion | |

| USD 52.3 Billion | |

| 9.6% | |

| North America | |

| Asia Pacific |

Customization Offered

Cross-segment Market Size and

Analysis

for Mentioned Segments

Cross-segment Market Size and

Analysis

for Mentioned Segments- Additional Company Profiles (Upto 5

With

No Cost)

- Additional Countries (Apart From

Mentioned Countries)

- Country/Region-specific Report

- Go To Market Strategy

- Region Specific Market Dynamics

- Region Level Market Share

- Import Export Analysis

- Production Analysis

- Others Request

Customization Speak To

Analyst

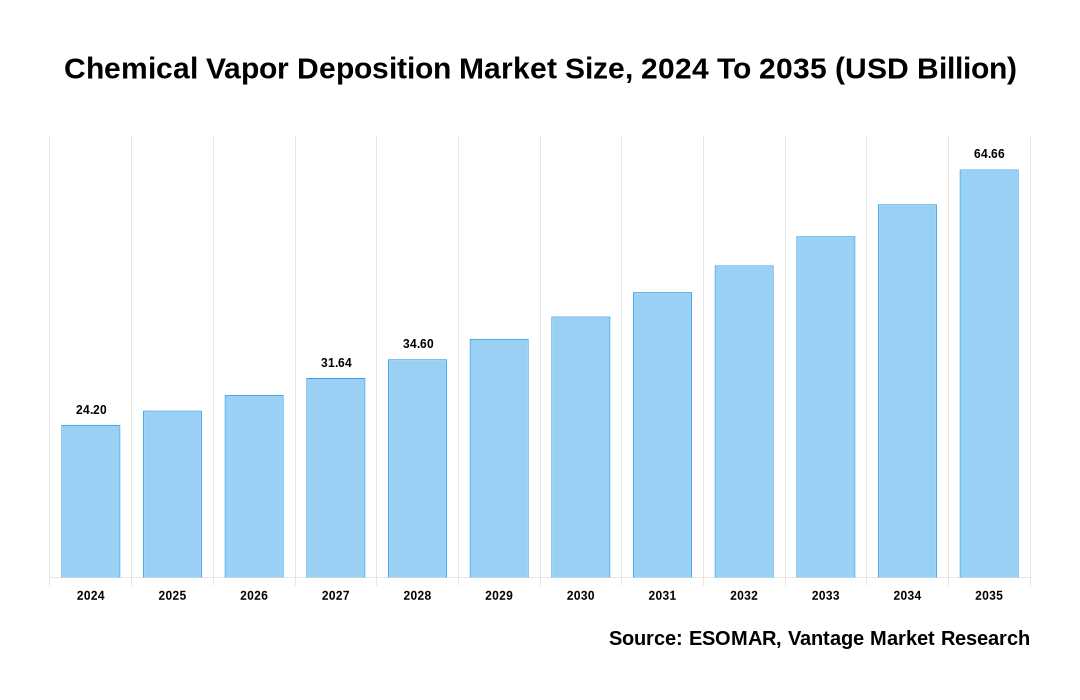

The global Chemical Vapor Deposition Market is valued at USD 22.91 Billion in 2023 and is projected to reach a value of USD 52.3 Billion by 2032 at a CAGR (Compound Annual Growth Rate) of 9.6% between 2024 and 2032. The global market is driven by increasing demand for high-performance coatings, rising applications in electronics & semiconductors, advancements in medical devices, and growing adoption in the automotive and aerospace industries.

Key Highlights

- Asia Pacific dominated the market in 2023, with 52.4% market share, driven by rapid growth in the electronics and semiconductor industries, particularly in countries like China, Japan, and South Korea

- In 2023, CVD Equipment segment dominated the market with a 66.3% share due to the advancements in equipment technology, increased demand for high-precision and high-performance coatings in electronics, semiconductors, and photovoltaics, and the growing adoption of CVD processes in emerging applications such as advanced materials and renewable energy solutions

- Based on Application, the Semiconductor & Microelectronics segment dominated the market in 2023, driven by increasing demand for high-performance and miniaturized electronic devices

- There is a growing emphasis on developing sustainable CVD processes that minimize environmental impact, reduce energy consumption, and utilize eco-friendly precursor materials

Chemical Vapor Deposition Market Size, 2023 To 2032 (USD Billion)

AI (GPT) is here !!! Ask questions about Chemical Vapor Deposition Market

Category Overview

Based on Category, the global market is segmented into CVD Equipment, CVD Materials, and CVD Services. The CVD Equipment segment dominated the global market with 66.3% of revenue share in 2023.

The CVD Equipment segment’s dominance is driven by the increasing need for advanced, high-performance materials used in industries such as semiconductors, optical coatings, and protective layers. Such materials are crucial for the development of innovative electronics, energy-efficient devices, and durable coatings. As the production of high-performance materials expands, the demand for CVD equipment is anticipated to grow throughout the forecast period.

On the other hand, the CVD services segment is expected to experience significant growth at a notable compound annual growth rate (CAGR). CVD services are essential within the Chemical Vapor Deposition market, providing thin film deposition solutions for various industries. Such services involve applying thin films onto substrates through chemical reactions in a gaseous state, enabling the creation of tailored materials with specific properties. As the semiconductor industry advances toward smaller, more complex components, CVD services are crucial for depositing ultra-thin & precise films on microchips, sensors, and integrated circuits. The increasing complexity and miniaturization of electronic devices are driving a substantial demand for these specialized CVD services.

Regional Overview

In 2023, Asia Pacific dominated the global market with a revenue share of 52.4%. In the Asia Pacific region, China stands out as the largest economy by GDP. Although the country has historically depended on coal for energy, recent years have seen a shift with the government closing mines and limiting new coal power plants, especially in densely populated areas. Despite these efforts, coal still constitutes 59% of China's electricity consumption. The nation's solar energy sector, driven by large-scale production and advancements in technology, aims to combat urban air pollution and enhance energy security, positioning China as a global leader in clean energy technologies. Major solar PV manufacturers like JinkoSolar, JA Solar, and Trina Solar are based in China, which saw its solar PV capacity increase from 253.4 GW in 2020 to 306.4 GW in 2023. Additionally, solar PV exports from China surpassed USD 30 billion in 2021, contributing significantly to the country’s trade surplus.

India's electronics industry is maintained by a growing middle class, rising disposable incomes, and increasing demand for high-end technology, alongside falling electronics prices. The Indian semiconductor sector, part of a rapidly expanding electronics system design & manufacturing industry, shows promising growth. From April to December 2022, electronic goods exports surged to USD 16.67 billion, a 51.56% increase from the previous year. Key exports include mobile phones, IT hardware, consumer electronics, industrial electronics, and auto electronics, with projections suggesting India's electronics exports could reach USD 120.03 billion by 2026.

In 2023, the North American CVD market held the second-largest market share. The region, home to major consumer electronics manufacturers, continues to see a rising demand for high-quality & advanced devices. CVD technology is crucial for producing sophisticated microelectronics, such as integrated circuits, sensors, and displays, which cater to the market's needs for miniaturization & enhanced performance. Additionally, there is a growing focus on developing 2D materials, like graphene, using CVD techniques. Graphene's remarkable mechanical, electrical, & thermal properties have made it highly sought after for applications in flexible electronics, sensors, and energy storage. The increased production of consumer electronics and advanced microelectronics is driving the heightened demand for CVD technology in North America.

Key Trends

- Rising Demand in Electronics and Semiconductors: Increasing use of CVD in semiconductor manufacturing for thin-film deposition, driven by growth in consumer electronics and IoT devices.

- Advancements in Nanotechnology: Enhanced applications in nanomaterial production for electronics, coatings, and biomedical devices.

- Growth in Solar Photovoltaics: Increasing adoption of CVD processes in the production of high-efficiency solar cells, spurred by demand for renewable energy.

- Emergence of Advanced Materials: Development of advanced materials like graphene and carbon nanotubes using CVD technology for various industrial applications.

- Technological Innovations in Coating Processes: Continuous advancements in CVD equipment and processes, including plasma-enhanced CVD and low-pressure CVD, improving efficiency and deposition quality.

Market Dynamics

Rising Demand for CVD in the Electronics Industry

The growing demand from the electronics industry has significantly boosted the use of Chemical Vapor Deposition (CVD) for producing thin films of semiconductors, conductors, and insulators. CVD is essential for fabricating advanced electronic materials & structures, including diffusion barriers and high thermal conductivity substrates. It employs various materials such as titanium nitride, silicon nitride, silicon oxide, diamond, and aluminum nitride. Aluminum has traditionally been favored for electrical conductors in semiconductor devices due to its low-temperature CVD processing, but copper has emerged as a superior alternative for IC metallization.

Recent advancements, particularly in Japan, have demonstrated that sub-quarter-micron copper interconnects can be produced using metallo-organic Chemical Vapor Deposition (MOCVD) and chemical mechanical polishing on a large scale. CVD copper competes with sputtering, the current dominant method for copper deposition. Additionally, CVD is extensively used to create thin films of electrical insulators like silicon oxide (SiO2) and silicon nitride (Si3N4). According to the Semiconductor Industry Association (SIA), the global semiconductor industry reached USD 574.1 billion in sales in 2022, with major players like Intel and Samsung Electronics generating substantial revenue. Meanwhile, the US consumer electronics market is projected to grow to nearly USD 505 billion by the end of 2022.

Advancements in Chemical Vapor Deposition (CVD): Transforming Material Processing and Expanding Market Opportunities

Chemical Vapor Deposition (CVD) synthesis & techniques have seen significant advancements, establishing themselves as a superior material processing technology compared to physical vapor deposition methods. The ability to tune deposition rates and achieve excellent conformality has propelled the use of CVD for high-end materials in the electronics and semiconductor industries. The integration of carbon nanotubes and graphene for next-generation electronics has broadened the market opportunities for CVD technologies. For instance, CVD synthesis is now used for high-performance flexible transparent electrodes.

Emerging techniques in substrate pretreatment and improvements in post-growth processes have further invigorated market growth. Favorable regulations supporting the use of low-dimensional materials in electronics manufacturing have also boosted demand. Advances in CVD instrumentation and the development of new materials chemistry have expanded revenue streams, while enhancements in gas delivery systems & thermal CVD processes have improved synthesis efficiency and application reach.

Challenges and Barriers to Entry in the CVD Market

A major barrier to entry in the CVD market is the substantial upfront investment needed for equipment and infrastructure. CVD systems are often costly to acquire, install, and maintain, posing challenges for smaller companies trying to enter the market. Additionally, CVD processes demand a high level of technical expertise and specialized knowledge. Operating and optimizing CVD equipment can be complex, requiring skilled personnel & extensive training. This complexity limits the accessibility of CVD technology to a narrower range of industries and businesses.

Report Coverage & Deliverables

Get Access Now

Track market trends LIVE & outsmart rivals with our Premium Data Intel Tool: Vantage Point

Competitive Landscape

The Chemical Vapor Deposition market is fiercely competitive, featuring companies that serve both regional & global customers. Major players in the market include ASM International NV, CVD Equipment Corporation, Aixtron SE, and Applied Materials Inc., among others. Companies are investing heavily in the development of new deposition techniques to boost equipment performance and efficiency. For instance, in May 2023, The GIA laboratory in Hong Kong evaluated the largest lab-grown diamond ever produced using Chemical Vapor Deposition (CVD). This 34.59-carat emerald-cut diamond, created by Ethereal Green Diamond in India, was graded as G color and VS2 clarity by the GIA. Additionally, top market players are expanding their manufacturing facilities to enhance production capacity, streamline supply chains, and shorten lead times.

Recent Market Developments

- In July 2023, OC Oerlikon Management AG has unveiled its newest PVD coating, BALIQ TISINOS PRO. This advanced coating is designed for use with hardened steels, stainless steels, and high-temperature alloys. By applying BALIQ TISINOS PRO, the load on tools is significantly reduced, resulting in substantial enhancements in wear resistance for steels with hardness levels up to 70 HRC during hard machining operations.

- In May 2023, AIXTRON has invested approximately 100 million euros (USD 109.7 million) in its Herzogenrath facility. This investment is intended to establish an innovation center aimed at significantly boosting the company's research & development capabilities.

- In February 2023, Veeco Instruments Inc. revealed that it acquired Epiluvac AB, a privately-owned producer of Chemical Vapor Deposition (CVD) epitaxy systems, on January 31, 2023. Epiluvac specializes in advanced silicon carbide (SiC) applications for the electric vehicle sector. The integration of Epiluvac's technology with Veeco's extensive global market presence is expected to be a major driver of long-term growth for Veeco.

- In April 2022, Applied Materials, Inc. has unveiled new innovations to support customers in advancing 2D scaling with EUV lithography and has showcased the industry's most comprehensive portfolio of technologies for manufacturing next-generation 3D Gate-All-Around (GAA) transistors.

- In November 2022, CVD Equipment Corporation has been awarded a USD 3.7 million contract in the aerospace sector for a production coating system featuring chemical vapor infiltration. This system is designed to deposit ceramic composite materials used in gas turbine engines and other aerospace components.

The global Chemical Vapor Deposition market can be categorized as Category, Application, and Region.

| Parameter | Details |

|---|---|

| Segments Covered |

By Category

By Application

By Region

|

| Regions & Countries Covered |

|

| Companies Covered |

|

| Report Coverage | Market growth drivers, restraints, opportunities, Porter’s five forces analysis, PEST analysis, value chain analysis, regulatory landscape, technology landscape, patent analysis, market attractiveness analysis by segments and North America, company market share analysis, and COVID-19 impact analysis |

| Pricing and purchase options | Avail of customized purchase options to meet your exact research needs. Explore purchase options |

FAQ

Frequently Asked Question

What is the global demand for Chemical Vapor Deposition in terms of revenue?

-

The global Chemical Vapor Deposition valued at USD 22.91 Billion in 2023 and is expected to reach USD 52.3 Billion in 2032 growing at a CAGR of 9.6%.

Which are the prominent players in the market?

-

The prominent players in the market are ASM International NV, Plasma-Therm LLC, Applied Materials Inc., CVD Equipment Corporation, Tokyo Electron Limited., Veeco Instruments Inc., OC Oerlikon Management AG, IHI Corporation, voestalpine AG, ULVAC Inc., Aixtron SE, RIBER, TAIYO NIPPON SANSO CORPORATION, Nuflare Technology Inc..

At what CAGR is the market projected to grow within the forecast period?

-

The market is project to grow at a CAGR of 9.6% between 2024 and 2032.

What are the driving factors fueling the growth of the market.

-

The driving factors of the Chemical Vapor Deposition include

Which region accounted for the largest share in the market?

-

Asia Pacific was the leading regional segment of the Chemical Vapor Deposition in 2023.