Chemical Intermediates Market

Chemical Intermediates Market - Global Industry Assessment & Forecast

210

2024

Nov - 2024

![]()

![]()

![]()

VMR-3230

Segments Covered

By

Product Type Alkylamines, Acetates, Diols & Glycols, Dicarboxylic Acids, Acrylic Acids, Others

By

Product Type Alkylamines, Acetates, Diols & Glycols, Dicarboxylic Acids, Acrylic Acids, Others

-

By

Function Solvents, Catalysts, Additives, Monomers, Stabilizers, Preservatives

-

By

Application Resin Production, Plastic Manufacturing, Surfactants & Detergents, Adhesives & Sealants, Lubricants, Others

-

By

End-Use Industry Pharmaceuticals, Agrochemicals, Textiles & Dyes, Paints & Coatings, Personal Care & Cosmetics, Chemicals & Polymers

-

By

Region North America, Europe, Asia Pacific, Latin America, Middle East & Africa

Snapshot

| 2024 | |

| 2025 - 2034 | |

| 2019 - 2023 | |

| USD 118.07 Billion | |

| USD 259.66 Billion | |

| 8.2% | |

| Asia Pacific | |

| Asia Pacific |

Customization Offered

Cross-segment Market Size and

Analysis

for Mentioned Segments

Cross-segment Market Size and

Analysis

for Mentioned Segments- Additional Company Profiles (Upto 5

With

No Cost)

- Additional Countries (Apart From

Mentioned Countries)

- Country/Region-specific Report

- Go To Market Strategy

- Region Specific Market Dynamics

- Region Level Market Share

- Import Export Analysis

- Production Analysis

- Others Request

Customization Speak To

Analyst

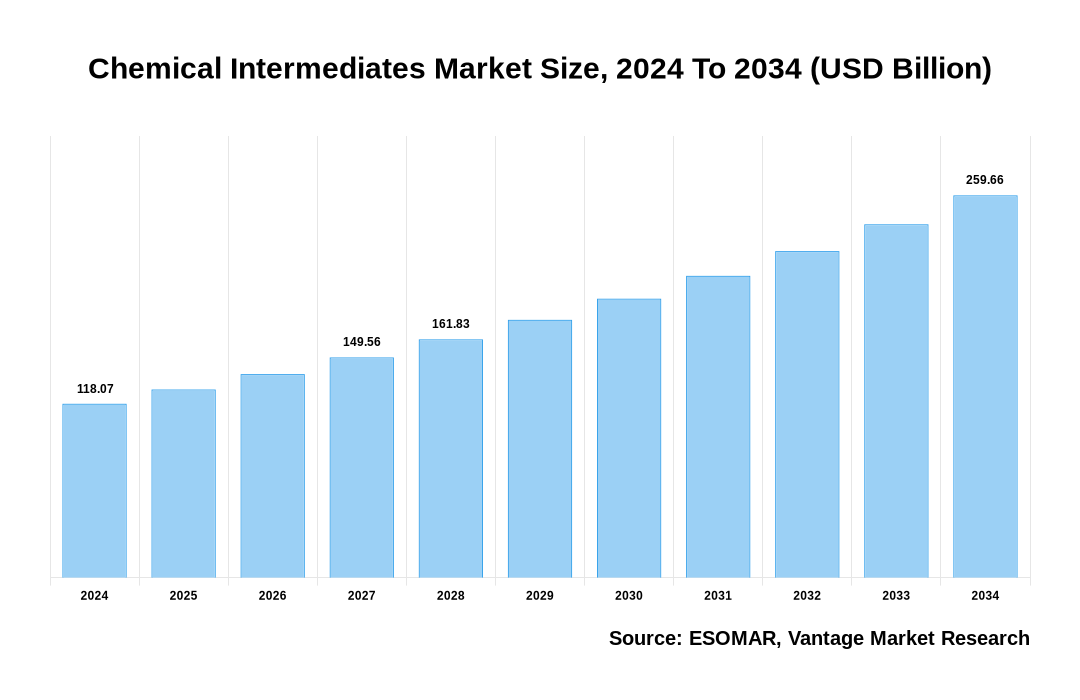

The global Chemical Intermediates market size was USD 109.12 billion in 2023, and is calculated at USD 118.07 Billion in 2024. The market is projected to reach USD 259.66 Billion by 2034, and register a revenue 8.2% over the forecast period (2025-2034).

Premium Insights:

Global Chemical Intermediates market growth is driven by factors such as rising demand from pharmaceuticals, agrochemicals, and automotive sectors, and increasing investments in sustainable, bio-based intermediates and advancements in specialty chemicals. Among the regional markets, the Asia Pacific Chemical Intermediates market accounted for over 50% share of global market revenue, led by high production, demand, and consumption of Chemical Intermediates across industries in China and India. Growth of the global Chemical Intermediates market is expected to incline significantly between 2025 and 2034, driven by trends such as increasingly stringent environmental regulations, steady shift toward greener solutions, and digitalization in chemical processes. Other factors include strategic mergers, capacity expansions, and Research and Development (R&D) initiatives by various companies focused on innovative applications and sustainability goals.

Chemical Intermediates play vital roles in the production of a variety of essential materials used across diverse industries and applications. Some products include alkylamines, acetates, diols & glycols, dicarboxylic acids, acrylic acids, and function as solvents, catalysts, additives, monomers, stabilizers, and preservatives. Chemical Intermediates are used in resin production, plastic manufacturing, manufacture of surfactants & detergents, adhesives & sealants, and lubricants, among other products.

Chemical Intermediates are widely used across industries including pharmaceuticals, agrochemicals, textiles & dyes, paints & coatings, personal care & cosmetics, chemicals & polymers, and others. Major industries in terms of demand and consumption volumes are pharmaceuticals, agrochemicals, automotive, textiles, and personal care.

Chemical Intermediates are synthesized from key raw materials such as petrochemicals, alcohols, and acids, serving as building blocks in the production of end products like medicines, pesticides, polymers, and dyes. The primary benefits of Chemical Intermediates is ability to enhance product performance, increase manufacturing efficiency, and facilitate innovations through specialized applications.

Advancements in sustainable production, such as bio-based intermediates, are reshaping the market, driven by increasingly stringent environmental and government regulations and rising demand for eco-friendly solutions. Leaders in the industry are adopting green chemistry practices, improving waste management, and exploring renewable feedstocks to align with global sustainability goals. In addition, digitalization and process automation are optimizing production cycles, reducing costs, and ensuring high-quality output.

Chemical Intermediates Market Size, 2024 To 2034 (USD Billion)

AI (GPT) is here !!! Ask questions about Chemical Intermediates Market

Top Chemical Intermediates Market Drivers and Trends:

- Diverse Applications Across End-Use Industries: Chemical Intermediates serve as essential building blocks in a wide range of formulations, products, and industries, including pharmaceuticals, agrochemicals, automotive, personal care, and textiles. These chemicals are used in the production of pharmaceuticals, fertilizers, dyes, and plastics, enabling the development of high-value end products. Growing need for specialty chemicals across these sectors and others, is a major factor driving market growth.

- Technological Advancements and Product Innovation: Innovations in chemical synthesis and production processes, such as green chemistry and bio-based intermediates, are enhancing product efficiency and environmental sustainability. Research and development efforts focusing on creation of high-performance intermediates for emerging technologies, such as Electric Vehicle (EV) batteries, advanced polymers, and specialty coatings, which driving market growth. Such advancements also align with the steady shift in the industry towards sustainable production.

- Rising Demand from High-Growth Markets: Asia Pacific is a high-growth market due to China, India, and Japan combines becoming a central hub for Chemical Intermediates, driven by rapid industrialization and favorable manufacturing conditions and policies in these countries. Rising consumer demand for pharmaceuticals, agrochemicals, and consumer goods in countries in the region is also driving up local production and attracting investments in capacity expansions, thereby supporting overall market growth.

- Environmental Regulations and Sustainability Initiatives: Increasingly stringent environmental regulations are encouraging adoption of eco-friendly intermediates, and reducing reliance on traditional, hazardous chemicals. This trend aligns with the broader shift towards sustainable manufacturing and circular economy practices, and is supporting demand for bio-based and biodegradable intermediates. Companies are also investing in green technologies and engaging in partnerships to meet regulatory requirements and consumer expectations.

Chemical Intermediates Market Restraining Factor Insights

- Volatility in Raw Material Prices and Supply Chain Disruptions: Chemical Intermediates are dependent on petrochemicals and other raw materials, the prices of which are subject to fluctuations due to crude oil price volatility, geopolitical tensions, and supply chain constraints. Unstable pricing creates challenges for manufacturers, increasing production costs and reducing profit margins. Also, disruptions in global supply chains such as restrictions and sanctions, or disrupted logistics transport as a result of geopolitical conflicts or disturbances can impact timely availability of raw materials, leading to delays and reduced market availability.

- Environmental Regulations and Compliance Costs: Rising environmental concerns and stricter regulatory frameworks around chemical production, emissions, and waste management are significant challenges for companies manufacturing Chemical Intermediates. Many intermediates are associated with hazardous by-products, requiring costly waste treatment processes to ensure regulatory compliance. Transitioning towards greener production methods, while necessary, requires substantial R&D investments and infrastructure upgrades, and this can potentially slow down adoption among companies without sufficient resources or with budget constraints.

- Competition from Bio-Based and Sustainable Alternatives: As industries shift towards sustainable practices, there is increasing pressure to replace conventional Chemical Intermediates with bio-based or eco-friendly alternatives. Governments, consumers, and industries alike are pushing for sustainable solutions, which could limit demand for traditional Chemical Intermediates. The development and commercialization of green alternatives are also being accelerated by investments in biotechnology and renewable resources, potentially impacting market share and revenue for conventional Chemical Intermediates over the long term.

Chemical Intermediates Market Opportunities

- Expansion through Mergers, Acquisitions, and Strategic Alliances: Companies can create new revenue streams by acquiring regional firms or forming joint ventures to diversify their product portfolios and expand market presence. Mergers and acquisitions provide access to innovative technologies and strengthen supply chains. For instance, the acquisition of specialty chemical firms allows leaders to penetrate niche markets, such as bio-based intermediates, accelerating growth.

- Product Innovation and Development of Sustainable Solutions: Rising demand for eco-friendly chemicals presents manufacturers with opportunity to focus on developing bio-based or biodegradable intermediates to meet regulatory requirements and consumer preferences. Investing in R&D to introduce high-performance, low-emission products can attract new customers, especially in sectors like pharmaceuticals, agrochemicals, and consumer goods. Innovating through digitalization — such as smart manufacturing and data-driven process optimization — can also boost production efficiency.

- Regional Market Penetration and Capacity Expansion: Targeting high-growth regions like Asia Pacific, where industrialization and consumer demand are increasing, offers lucrative opportunities. Establishing manufacturing facilities in emerging markets enables companies to reduce production costs and shorten supply chains. Also, forming strategic supply agreements with local players ensures stable raw material availability and reduces operational risks.

Chemical Intermediates Market Segmentation:

By Product Type:

- Alkylamines

- Acetates

- Diols & Glycols

- Dicarboxylic Acids

- Acrylic Acids

- Others

By Function:

- Solvents

- Catalysts

- Additives

- Monomers

- Stabilizers

- Preservatives

By Application:

- Resin Production

- Plastic Manufacturing

- Surfactants & Detergents

- Adhesives & Sealants

- Lubricants

- Others

By End-Use Industry:

- Pharmaceuticals

- Agrochemicals

- Textiles & Dyes

- Paints & Coatings

- Personal Care & Cosmetics

- Chemicals & Polymers

Chemical Intermediates Market Segment Insights:

By Product Type:

The diols and glycols segment is expected to account for largest revenue share among the product type segments over the forecast period due to wide use in the production of polyurethanes and polyester resins. These materials are essential in industries such as automotive, textiles, and packaging, and increasing production of vehicles, fabrics, and packaging materials is driving growth of this segment to a major extent. Demand for lightweight materials in automotive manufacturing, as well as the expanding use of polyethylene terephthalate in packaging, especially for beverages, is also supporting revenue growth. Also, diols and glycols are key intermediates in producing antifreeze and coolants, which are registering steady demand from the automotive and construction industries.

By Function:

The solvents segment is expected to continue to dominate other function segments over the forecast period. This can be attributed to extensive usage of solvents across multiple industries, including pharmaceuticals, paints, and personal care. In the pharmaceutical sector, solvents are crucial for drug synthesis and formulations, and in the paints and coatings industry, are used for achieving desired viscosity and drying properties. Rapid growth of construction and automotive sectors is also a major factor driving demand for a variety of end-products that are dependent on solvents during manufacturing.

By Application:

The plastic manufacturing segment is expected to account for largest revenue share among the application segments over the forecast period. Intermediates are widely used in the production of a number of essential polymers such as polyethylene, polypropylene, and polyvinyl chloride. Rising consumer demand for packaging, electronics, and automotive components, coupled with inclining focus on sustainable and biodegradable plastics is supporting growth of this segment, and also opening up new avenues for use of various Chemical Intermediates.

Report Coverage & Deliverables

Get Access Now

Track market trends LIVE & outsmart rivals with our Premium Data Intel Tool: Vantage Point

By End-Use Industry:

The pharmaceutical segment among the end-use industry segments is expected to account for largest revenue share over the forecast period. Factors such as increasing R&D initiatives and need for specialized Chemical Intermediates in drug formulations are supporting growth of this segment to a major extent. Also, rising global healthcare spending and continuous development of new therapies is supporting demand for intermediates like alkylamines and acetates. Also, expansion of generic drug manufacturing, especially in emerging economies, is further contributing to demand for Chemical Intermediates.

Regions and Countries

North America

- United States

- Canada

- Mexico

Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

Asia Pacific

- China

- Japan

- India

Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

Rest of Latin America

- Middle East & Africa

- Saudi Arabia

- South Africa

- United Arab Emirates

- Israel

- Rest of MEA

Chemical Intermediates Market Regional Landscape:

Among the regional markets, Asia Pacific Chemical Intermediates market accounted for a revenue share of over 50% in the global market in 2023. Major revenue contributors are China, India, and Japan, attributed to rapid industrialization and increasing demand for specialty chemicals across sectors such as pharmaceuticals, agrochemicals, and manufacturing.

North America Chemical Intermediates market accounted for second-largest revenue share in the global market in 2023, with majority revenue contribution from the US. Advancements in petrochemical production and strong R&D capabilities in the US and increasing investments in various industries are key factors supporting market growth. Europe Chemical Intermediates market growth is driven by robust chemical industries in Germany and France. Factors including rising demand from pharmaceuticals and agriculture for Chemical Intermediates, increasing disease prevalence and R&D initiatives in healthcare sector, expansion of plastics and petrochemical industries and technological innovations and sustainability initiatives are expected to continue to support growth of the Europe market.

In Latin America, Brazil and Mexico have been registering steady incline in demand for various chemicals, especially agricultural chemicals. Some common factors across the regional markets include increased demand from pharmaceutical and agrochemical industries, shift towards sustainable and bio-based intermediates, and expansion of downstream industries, such as automotive and consumer goods.

Chemical Intermediates Market Competitive Landscape:

Company List:

- BASF

- Sinopec

- Dow

- SABIC

- INEOS

- LG Chem

- LyondellBasell

- Mitsubishi Chemical Group

- Evonik Industries

- Reliance Industries

- ExxonMobil Chemical

- Air Liquide

- Sumitomo Chemical

- Wanhua Chemical Group

- Formosa Plastics

Competitive Landscape:

The competitive landscape in the global Chemical Intermediates market is highly dynamic, with both large multinational corporations and regional firms competing in an evolving market. Leading companies, such as BASF, Dow, and Sinopec, rely on diversified portfolios and economies of scale to stay competitive. Smaller players, meanwhile, focus on niche markets, particularly in specialty intermediates, to differentiate themselves. Companies are deploying strategies such as vertical integration to streamline production and secure raw material supply chains. Merger and acquisition is another strategy to expand product offerings, access new technologies, and penetrate emerging markets.

Sustainability and innovation are also major focal points, with major companies investing substantially in R&D to develop bio-based and environmentally friendly intermediates, in response to increasingly stringent regulations and rising consumer demand for greener solutions. Partnerships with research institutions and technology providers is also enabling companies to engage in innovation and product enhancements. In addition, geographic expansion, particularly into high-growth regions such as Asia Pacific, enables companies to tap into new consumer bases and benefit from lower production costs.

Recent Developments

- October 25, 2024: BASF Petronas Chemicals Sdn Bhd (BPC), which is a joint venture between BASF and Petroliam Nasional Bhd (Petronas), announced successful doubling of annual production capacity of 2-ethylhexanoic acid (2-EHAcid) at the integrated site in Kuantan, Pahang, Malaysia, to 60,000 tons from 30,000 tons. The company increased production capacity of 2-EHAcid, which is a chemical intermediate used as a compound in the production of synthetic lubricants as well as oil additive, in order to cater to rising demand from various industries, including demand for functional fluids like automotive coolants, and metal salts for paint dryers, plasticizers, stabilizers, catalysts and others. In addition to the production site in Kuantan, BASF produces 2-EHAcid at its Verbund site in Ludwigshafen, Germany, and expansion in Kuantan will enable the company to cater to rapidly rising demand for high-quality 2-ethylhexanoic acid in Asia Pacific.

- March 4, 2024: International Chemical Investors Group (ICIG) finalized the acquisition of a majority stake in Vasant Chemicals, which is a well-established Indian manufacturer of specialty chemicals and pharmaceutical intermediates. Vasant Chemicals will now operate under the WeylChem Group, ICIG's fine chemicals division. This acquisition is part of WeylChem’s broader strategy to strengthen its presence in the global specialty chemicals sector. For Vasant Chemicals, this partnership offers a valuable opportunity to expand its global reach and enhance the value it delivers to customers. By combining the strengths of both companies — such as expertise, advanced technologies, and resources — the acquisition is expected to generate sustainable long-term benefits for customers, employees, and stakeholders alike. The integration also aligns with ICIG’s strategic priorities, focusing on growth through collaboration and innovation within the specialty chemicals market.

Frequently Asked Questions:

Q: What is the global Chemical Intermediates market size in 2024 and what is the projection for 2034?

A: The global Chemical Intermediates market size was calculated at USD 118.07 billion in 2024 and expected to reach USD 259.66 billion 2034

Which regional market accounted for largest revenue share in 2023, and what is the expected trend over the forecast period?

A: Asia Pacific accounted for largest revenue share in the global market in 2023, and is expected to continue to maintain its lead during the forecast period.

Q: Which are the major companies are included in the global Chemical Intermediates market report?

A: Major companies in the Chemical Intermediates market report are BASF, Sinopec, Dow, SABIC, INEOS, LG Chem, LyondellBasell, Mitsubishi Chemical Group, Evonik Industries, Reliance Industries, ExxonMobil Chemical, Air Liquide, Sumitomo Chemical, Wanhua Chemical Group, Formosa Plastics.

Q: What is the projected revenue CAGR of the global Chemical Intermediates market over the forecast period?

A: The global Chemical Intermediates market is expected to register a CAGR of 8.2% between 2025 and 2034.

Q: What are some key factors driving revenue growth of the Chemical Intermediates market ?

A: Some key factors driving market revenue growth are rising demand from pharmaceuticals, agrochemicals, and automotive sectors, increasing investments in sustainable, bio-based intermediates, advancements in specialty chemicals, steady shift toward greener solutions, and digitalization in chemical processes.

FAQ

Frequently Asked Question

What is the global demand for Chemical Intermediates in terms of revenue?

-

The global Chemical Intermediates valued at USD 118.07 Billion in 2024 and is expected to reach USD 259.66 Billion in 2034 growing at a CAGR of 8.2%.

Which are the prominent players in the market?

-

The prominent players in the market are BASF, Sinopec, Dow, SABIC, INEOS, LG Chem, LyondellBasell, Mitsubishi Chemical Group, Evonik Industries, Reliance Industries, ExxonMobil Chemical, Air Liquide, Sumitomo Chemical, Wanhua Chemical Group, Formosa Plastics..

At what CAGR is the market projected to grow within the forecast period?

-

The market is project to grow at a CAGR of 8.2% between 2025 and 2034.

What are the driving factors fueling the growth of the market.

-

The driving factors of the Chemical Intermediates include

Which region accounted for the largest share in the market?

-

Asia Pacific was the leading regional segment of the Chemical Intermediates in 2024.