Aerostructures Market

Aerostructures Market - Global Industry Assessment & Forecast

156

2022

Nov - 2023

![]()

![]()

![]()

VMR-2340

Segments Covered

By

Component Fuselages, Empennages, Wings, Noses, Nacelles & Pylons, Doors & Skids, Flight Control Surfaces

By

Component Fuselages, Empennages, Wings, Noses, Nacelles & Pylons, Doors & Skids, Flight Control Surfaces

-

By

Material Composites, Alloys & Superalloys, Metals

-

By

Aircraft Type Commercial Aviation, Business & General Aviation, Military Aviation, Unmanned Aerial Vehicles, Advanced Air Mobility

-

By

End Use OEM, Aftermarket

-

By

Region North America, Europe, Asia Pacific, Latin America, Middle East & Africa

Snapshot

| 2022 | |

| 2023 - 2030 | |

| 2017 - 2021 | |

| USD 60.4 Billion | |

| USD 103 Billion | |

| 6.9% | |

| Asia Pacific | |

| North America |

Customization Offered

Cross-segment Market Size and

Analysis

for Mentioned Segments

Cross-segment Market Size and

Analysis

for Mentioned Segments- Additional Company Profiles (Upto 5

With

No Cost)

- Additional Countries (Apart From

Mentioned Countries)

- Country/Region-specific Report

- Go To Market Strategy

- Region Specific Market Dynamics

- Region Level Market Share

- Import Export Analysis

- Production Analysis

- Others Request

Customization Speak To

Analyst

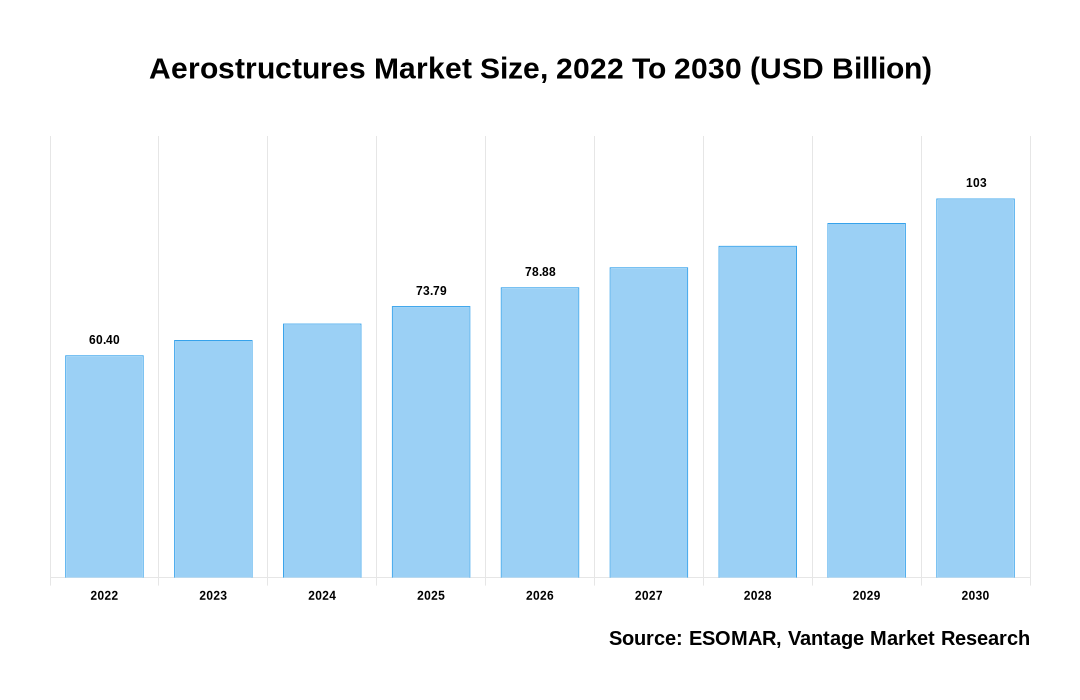

The global Aerostructures Market is valued at USD 60.4 Billion in 2022 and is projected to reach a value of USD 103 Billion by 2030 at a CAGR (Compound Annual Growth Rate) of 6.9% between 2023 and 2030.

Premium Insights

Aerostructures is a component of the aircraft's airframe that is made separately. These are the critical components that allow treated aircraft to fly and stand in the face of shifting aerodynamic forces. Aerostructures are built to endure extreme weather conditions as well as structural fatigue caused by extreme loading cycles or bird strikes. Aerostructures are made from a variety of materials, including composites, alloys, metals, and superalloys, depending on their qualities and performance. The OEM segment is expected to increase fast during the projection period due to the increasing aftermarket services supplied by various Aerostructures manufacturers. The increase in commercial aircraft deliveries around the world is growing in the aircraft Aerostructures industry. With the increase in passenger flexibility in recent years, the commercial aviation industry has seen a significant increase in the deployment rate of commercial aircraft, which is driving the expansion of the global Aerostructures market. However, issues associated with composite materials, such as material recycling, are a major factor impeding the growth of the Aerostructures industry.

Aerostructures Market Size, 2022 To 2030 (USD Billion)

AI (GPT) is here !!! Ask questions about Aerostructures Market

- The global population growth and increased demand for passenger and cargo air services is growing the Aerostructures market during the projection period from 2023 to 2030.

- The fuselages segment will continue to dominance by component, capturing the largest market share globally throughout the forecast period 2023 to 2030.

- In 2022, North America has the largest growth rate, achieving the highest revenue share of 40.60%.

- The Asia Pacific region is expected to have the largest Compound Annual Growth Rate (CAGR) between 2023 and 2030.

Top Market Trends

- Unmanned Aerial Vehicles have grown in popularity in a variety of applications, including surveillance, agriculture, delivery services, infrastructure inspection, and military surveillance. As the demand for UAVs grows, so does the requirement for specialized Aerostructures that can resist the particular challenges of unmanned flight. This creates a specialized market for Aerostructures producers to provide lightweight, long-lasting components for unmanned platforms.

- Aerostructures Component original equipment manufacturers (OEMs) have begun to integrate developing technologies for efficient component production, such as 3D printing. Other technologies, such as machine learning, which are utilized in the production and integration of 3D printing, aid in the production, design, and manufacture of Aerostructures and create a complete component using a 3D model. These supportive measures have helped to boost market growth and attract investment in the Aerostructures industry.

- Due to its relative features, such as durability, dependability, and toughness, OEMs prefer composite materials to produce airplane airframes. Glass-reinforced plastics (GRP) and fiber-reinforced plastics (FRP) are composites that are primarily utilized to make the aircraft's skin and exterior layers.

- A chevron nozzle, a triangle pattern exhaust nozzle extension that helps minimize noise and is standard on current jets, is in high demand. Chevron is used to lower acoustic levels in emissions. This technology is used by modern generation Boeing 747 and 787 aircraft and has been shown to reduce fan tones by roughly 15 decibels. The teeth-like form of the muzzle lowers pressure variance, which in turn reduces jet noise. Chevron nozzle is helping to accelerate the growth of the Aerostructures market and drive innovation.

- The Aerostructures industry has been attracting significant composites and additive manufacturing methods, which have significantly altered global airframe design and aftermarket requirements. Demand for higher production rates, REACH compliance requirements, and non-conformities all have a substantial impact on airframe structural design and build procedures. These new technologies scale up production and expand market reach, further driving growth in the Aerostructures market.

- The aviation industry is growing. On millions of commercial flights each year, airlines around the world move billions of people and millions of tonnes of freight. While this is an indication of the significant economic influence of aviation on the global economy, it is worth noting that aviation accounts for more than 3% of global GDP. Further boosting market growth.

Report Coverage & Deliverables

Get Access Now

Economic Insights

The air transport business has a significant economic influence, both directly and as a facilitator of other industries. Its contribution includes direct, indirect, and induced effects on the total revenue of the air transport business. Because of the shutdown, there has been a fall in aircraft deliveries, which has resulted in a decrease in the manufacturing of Aerostructures components. The commercial aviation industry saw a significant decrease in aircraft deliveries in 2020. The COVID-19 epidemic had a significant impact on the world's two largest commercial aircraft manufacturers' annual orders and delivery. For example, global deliveries in 2020 were 723 aircraft, 42% lower than in 2019 and 55.3% lower than in 2018, marking the second straight year of decline. However, the market has outgrown the drop over the last few years and will be able to return to pre-pandemic demand due to increased passenger travel.

Market Segmentation

The Global Aerostructures Market is categorized into the below-mentioned segments as:

The global Aerostructures market can be categorized into Component, Material, Aircraft Type, End Use, Region. The Aerostructures market can be categorized into Fuselages, Empennages, Wings, Noses, Nacelles & Pylons, Doors & Skids, Flight Control Surfaces based on Component. The Aerostructures market can be categorized into Composites, Alloys & Superalloys, Metals based on Material. The Aerostructures market can be categorized into Commercial Aviation, Business & General Aviation, Military Aviation, Unmanned Aerial Vehicles, Advanced Air Mobility based on Aircraft Type. The Aerostructures market can be categorized into OEM, Aftermarket based on End Use. The Aerostructures market can be categorized into North America, Europe, Asia Pacific, Latin America, Middle East & Africa based on Region.

Based on Product Type

Fuselages to Lead Maximum Market Share Because Of Increased Commercial And Military Aircraft Production

In 2022, the Fuselages segment is poised to dominate the global market for Aerostructures. The fuselage is the main body part of the airplane that houses the cabin and cargo. The high cost of the aircraft's body construction is a major factor in the market domination of fuselage components. These constructions require sophisticated processes that necessitate consistent attention to safety, weight reduction, and effective aerodynamics. Companies that specialize in fuselage components not only contribute considerably to industry breakthroughs but also seek greater fuel efficiency, lower environmental impact, and improved passenger comfort. These advancements help to design aircraft and spacecraft that are not only more efficient but also more sustainable. They are at the cutting edge of modern aviation and space exploration.

Based on Application

Alloys and Superalloys Segment Expects Dominion, Owing to the Growing Demand for Alloy Materials Utilized In Major Airplane Components

In 2022, the Alloys and Superalloys segment will dominate the Aerostructures market because of the increased demand for alloy materials utilized in major airplane components. Aerospace alloys include Al and Mg alloys, as well as Ni, Co, and Ti alloys. In aluminum-based alloys and alloying elements such as copper, zinc, manganese, silicon, and magnesium, Al is the dominant metal in the system. Aerospace engineers and manufacturers rely on specific alloys, which are frequently created from metal alloys such as aluminum, titanium, and nickel. They are used in important parts such as wings, fuselages, landing gear, and engine sections.

Based on Region

North America to Dominate Global Sales Owing to Strong Presence Of Major Aerostructures Manufacturers and an Increase in Aircraft Orders And Deliveries

In 2022, the North American region emerged as the dominant player in the Aerostructures market. Because of the existence of key OEMs and a rising market. For example, in June 2023, the US government approved the sale of 16 surveillance aircraft to Canada for USD 6 billion. Similarly, increased commercial airline demand is catalyzing the industry in North America. For example, due to the increase in their business activities, Air Canada has received more than 15 new aircraft since January 2022. Within this region, there is a broad market that includes several enterprises involved in Aerostructures manufacturing and supply, which contribute to both commercial and defense aviation sectors.

The Aerostructures industry in the Asia Pacific region is rapidly growing in popularity due to the expanding number of OEMs in the region. The region has recently seen increased demand due to an increase in UAV applications. The market's expansion is fueled further by favorable government initiatives and an expanding defense budget. The region's commercial and military aircraft development and purchase projects are expected to accelerate market growth.

Competitive Landscape

The global Aerostructures market is highly competitive, with various key players operating in the industry. Some of the major companies in the market include AAR Corp (U.S.), Bombardier Inc. (U.S.), SAAB AB (Sweden), Spirit Aerosystems Inc. (U.S.), Triumph Group Inc. (U.S.), Cyient Ltd (India), Elbit Systems Ltd (Israel), GKN Aerospace (U.K.), Leonardo SpA (Italy), The Boeing Company (U.S.), Airbus SAS ( France). These companies are focusing on research and development activities to develop innovative and sustainable products. Additionally, strategic alliances, mergers, and acquisitions are frequent in the market as companies aim to expand their product offerings and market presence.

The key players in the global Aerostructures market include - AAR Corp (U.S.), Bombardier Inc. (U.S.), SAAB AB (Sweden), Spirit Aerosystems Inc. (U.S.), Triumph Group Inc. (U.S.), Cyient Ltd. (India), Elbit Systems Ltd. (Israel), GKN Aerospace (UK), Leonardo SPA (Italy), The Boeing Company (U.S.), Airbus SAS (France) among others.

Recent Market Developments

- In May 2023, The famed Massachusetts Institute of Technology presented a technological innovation and low-cost development to reinforce important materials used in aerospace and energy generation today.

- In April 2023, Leonardo SpA, an Italian aerospace and aircraft corporation, announced a collaboration with Cisco Technology to create cooperative technology initiatives. The collaboration intends to create cooperative goods and solutions as part of a green transition to safe logistics and transportation systems.

- In February 2033, Heart Aerospace, a Swedish electric aircraft developer, was named as a long-term partner for the air-New Zealand next-generation mission aircraft cooperation. The collaboration will aid in the replacement of the airline's Q300 domestic fleet.

Segmentation of the Global Aerostructures Market

| Parameter | Details |

|---|---|

| Segments Covered |

By Component

By Material

By Aircraft Type

By End Use

By Region

|

| Regions & Countries Covered |

|

| Companies Covered |

|

| Report Coverage | Market growth drivers, restraints, opportunities, Porter’s five forces analysis, PEST analysis, value chain analysis, regulatory landscape, technology landscape, patent analysis, market attractiveness analysis by segments and North America, company market share analysis, and COVID-19 impact analysis |

| Pricing and purchase options | Avail of customized purchase options to meet your exact research needs. Explore purchase options |

FAQ

Frequently Asked Question

What is the global demand for Aerostructures in terms of revenue?

-

The global Aerostructures valued at USD 60.4 Billion in 2022 and is expected to reach USD 103 Billion in 2030 growing at a CAGR of 6.9%.

Which are the prominent players in the market?

-

The prominent players in the market are AAR Corp (U.S.), Bombardier Inc. (U.S.), SAAB AB (Sweden), Spirit Aerosystems Inc. (U.S.), Triumph Group Inc. (U.S.), Cyient Ltd. (India), Elbit Systems Ltd. (Israel), GKN Aerospace (UK), Leonardo SPA (Italy), The Boeing Company (U.S.), Airbus SAS (France).

At what CAGR is the market projected to grow within the forecast period?

-

The market is project to grow at a CAGR of 6.9% between 2023 and 2030.

What are the driving factors fueling the growth of the market.

-

The driving factors of the Aerostructures include

- Growing Demand for Chevron Nozzle Supports Market Growth

Which region accounted for the largest share in the market?

-

North America was the leading regional segment of the Aerostructures in 2022.