Additive Manufacturing Market

Additive Manufacturing Market - Global Industry Assessment & Forecast

150

2022

Dec - 2023

![]()

![]()

![]()

VMR-2349

Segments Covered

By

Component Hardware, Software, Services

By

Component Hardware, Software, Services

-

By

Printer Type Desktop 3D Printer, Industrial 3D Printer

-

By

Technology Stereolithography, Fuse Deposition Modeling, Selective Laser Sintering, Direct Metal Laser Sintering, Polyjet Printing, Inkjet Printing, Electron Beam Melting, Laser Metal Deposition, Digital Light Processing, Laminated Object Manufacturing, Other Technologies

-

By

Software Design Software, Inspection Software, Printer Software, Scanning Software

-

By

Application Prototyping, Tooling, Functional Parts

-

By

Vertical Industrial Additive Manufacturing, Desktop Additive Manufacturing

-

By

Material Polymer, Metal, Ceramic

-

By

Region North America, Europe, Asia Pacific, Latin America, Middle East & Africa

Snapshot

| 2022 | |

| 2023 - 2030 | |

| 2017 - 2021 | |

| USD 14.5 Billion | |

| USD 69.3 Billion | |

| 21.6% | |

| Asia Pacific | |

| North America |

Customization Offered

Cross-segment Market Size and

Analysis

for Mentioned Segments

Cross-segment Market Size and

Analysis

for Mentioned Segments- Additional Company Profiles (Upto 5

With

No Cost)

- Additional Countries (Apart From

Mentioned Countries)

- Country/Region-specific Report

- Go To Market Strategy

- Region Specific Market Dynamics

- Region Level Market Share

- Import Export Analysis

- Production Analysis

- Others Request

Customization Speak To

Analyst

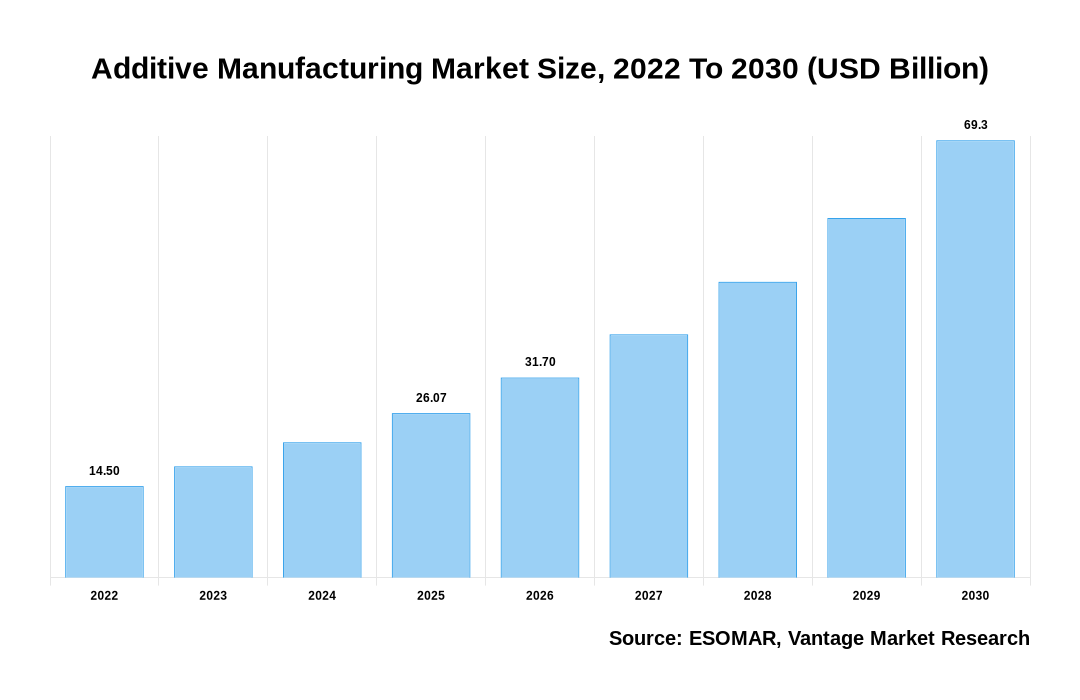

The global Additive Manufacturing Market is valued at USD 14.5 Billion in 2022 and is projected to reach a value of USD 69.3 Billion by 2030 at a CAGR (Compound Annual Growth Rate) of 21.6% between 2023 and 2030.

Premium Insights

The market for Additive Manufacturing is expanding rapidly, mostly due to the growing need across a range of industries for quick prototyping and customization. The aerospace and automotive industries' embrace of Additive Manufacturing technologies to produce lightweight and complicated components, which improves performance and fuel efficiency, is credited with this increase. Moreover, the medical and healthcare sector has embraced Additive Manufacturing to produce prosthetics and implants tailored to each patient, highlighting the market's adaptability. Further driving market expansion are the expanding uses of 3D printing in consumer goods, architecture, and electronics, as well as the increasing availability of innovative materials. In the upcoming years, the Additive Manufacturing industry is expected to experience substantial expansion and constant innovation due to the construction of supporting legislative frameworks and ongoing technological advancements.

Additive Manufacturing Market Size, 2022 To 2030 (USD Billion)

AI (GPT) is here !!! Ask questions about Additive Manufacturing Market

- The increasing demand for rapid prototyping and customized manufacturing across various industries is a significant driver for the {keyword}} market.

- The stereolithography segment will continue to assert its dominance by material, capturing the largest market share globally throughout the forecast period 2023 to 2030.

- In 2022, North America exhibited its market prowess, achieving the highest revenue share of over 35.6%.

- The Asia Pacific region is poised for remarkable growth, displaying a noteworthy Compound Annual Growth Rate (CAGR) between 2023 and 2030.

Top Market Trends

- The growing emphasis on sustainability in the Additive Manufacturing business is a notable trend that is still present. Manufacturers are looking into eco-friendly materials and procedures as environmental worries increase. This development is consistent with the movement toward circular economies, where 3D printing may cut waste by optimizing material use and recycling. Organizations are presently investigating bio-based and recycled materials to reduce Additive Manufacturing's carbon footprint, which is essential for fulfilling sustainability targets across a range of sectors.

- The use of simulation and digital twins in Additive Manufacturing is another noteworthy trend. With the use of this technology, physical products can be virtually replicated, facilitating extensive testing and optimization before actual manufacture. Through the simulation of the printing process and material behavior, producers may lower costs, improve product quality, and minimize faults. This tendency is especially important for sectors like aerospace and automotive, where accuracy and dependability are critical to the entire expansion and effectiveness of the business.

Report Coverage & Deliverables

Get Access Now

Economic Insights

The COVID-19 pandemic has had a major impact on the industry for Additive Manufacturing and its economic insights. At first, the pandemic caused supply chain disruptions, which resulted in a brief lull in the industry as production was either stopped or reduced. But it also highlighted how versatile and robust Additive Manufacturing is. Data from the Additive Manufacturing Users Group (AMUG) show that during the epidemic, several businesses swiftly redirected their attention to employing 3D printing technology to provide essential medical supplies, showcasing the industry's adaptability in handling crises. In addition, the pandemic's financial restrictions forced a reassessment of economical manufacturing techniques, with Additive Manufacturing drawing interest for its capacity to lower supply chain risks and facilitate local production. Although COVID-19 presented some initial difficulties, it also spurred innovation. It demonstrated the strategic value of Additive Manufacturing in responding to unanticipated changes, ultimately creating favorable long-term growth prospects for the industry.

Market Segmentation

Additive Manufacturing The global Additive Manufacturing market can be categorized into Component, Printer Type, Technology, Software, Application, Vertical, Material, Region. The Additive Manufacturing market can be categorized into Hardware, Software, Services based on Component. The Additive Manufacturing market can be categorized into Desktop 3D Printer, Industrial 3D Printer based on Printer Type. The Additive Manufacturing market can be categorized into Stereolithography, Fuse Deposition Modeling, Selective Laser Sintering, Direct Metal Laser Sintering, Polyjet Printing, Inkjet Printing, Electron Beam Melting, Laser Metal Deposition, Digital Light Processing, Laminated Object Manufacturing, Other Technologies based on Technology. The Additive Manufacturing market can be categorized into Design Software, Inspection Software, Printer Software, Scanning Software based on Software. The Additive Manufacturing market can be categorized into Prototyping, Tooling, Functional Parts based on Application. The Additive Manufacturing market can be categorized into Industrial Additive Manufacturing, Desktop Additive Manufacturing based on Vertical. The Additive Manufacturing market can be categorized into Polymer, Metal, Ceramic based on Material. The Additive Manufacturing market can be categorized into North America, Europe, Asia Pacific, Latin America, Middle East & Africa based on Region.

Based on Component

Hardware Components to Accommodate the Maximum Sales due to Widening Demand

Hardware is a product that is fully utilized in the Additive Manufacturing market. Numerous factors contribute to this supremacy. First, hardware refers to the actual 3D printers and associated machinery needed for Additive Manufacturing procedures. It serves as the cornerstone and structural support of any Additive Manufacturing process. Second, the demand for hardware is still being driven by ongoing developments in technology, which include wider material compatibility, improved precision, and quicker printing speeds. Furthermore, the growing use of 3D printing in a variety of industries, such as consumer products, automotive, aerospace, and healthcare, calls for the ongoing development and growth of hardware infrastructure. Finally, a large range of solutions that meet different needs and budgets are produced by the competitive landscape among hardware producers, which contributes to its dominant usage in the ecosystem of Additive Manufacturing.

Based on the Printer Type

Industrial 3D Printers to Accommodate Massive Sales Due to Supreme Precision Over its Counterparts

In 2022, the industry leader in Additive Manufacturing is an industrial 3D printer. This supremacy is the result of multiple important reasons. Compared to desktop models, industrial 3D printers are more precise, can produce greater quantities, and can deal with a wider variety of materials. They are designed to satisfy the demanding requirements of sectors where complicated and large-scale production is typical, like aerospace, automotive, healthcare, and engineering. Because of their strength and adaptability, industrial 3D printers are the industry standard for rapid prototyping, customized manufacturing, and mass production. This solidifies their place as the top option for Additive Manufacturing. Their ability to manufacture functional, high-quality parts on a commercial scale, together with continuous technological innovation, guarantees their dominance in the market.

Based on Technology

SLA to the Dominant Mode of Utilization due to a Greater Surface Finish

In 2022, Stereolithography (SLA) is one of the Additive Manufacturing technologies that is most widely used for a few strong reasons. SLA is preferred because of its great precision and flawless surface finish, which makes it perfect for applications like jewelry, dental models, and prototypes where precise features and smooth surfaces are essential. It uses a UV laser to cure photopolymer resin, which enables the fabrication of intricate and very accurate geometries. Continuous innovation has also led to the creation of quicker and more dependable machines, a wider variety of suitable materials, and enhanced automation features for SLA technology. Stereolithography is a widely used Additive Manufacturing method in both industrial and commercial contexts because of its accuracy, versatility, and continuous development.

Based on Software

Design-based Software to Maximize their Footprint due to their Crucial Functionality

In 2022, as the most popular product in the Additive Manufacturing business, design software is essential. The crucial part that design software plays in the whole Additive Manufacturing workflow is the reason for its supremacy. Design software enables users to precisely design complex and personalized items by enabling the creation of 3D models and digital prototypes. Engineers, designers, and manufacturers can improve designs for Additive Manufacturing with its user-friendly interfaces and advanced features, guaranteeing that components are appropriate for 3D printing techniques. Moreover, simulation tools are frequently integrated into design software to assist in finding and fixing possible problems before they are printed, saving time and money. Design software is at the forefront of the Additive Manufacturing business thanks to its ongoing development, which has improved compatibility with a range of 3D printers and materials and enabled users to utilize 3D printing technology fully.

Based on Application

Prototyping Applications to Widen in Growth Owing to their Ability to Quickly Produce Physical Moulds

In 2022, in the market for Additive Manufacturing, the product category that is most frequently used is prototyping. This is mainly because designers and engineers can quickly produce physical prototypes of new items or components thanks to Additive Manufacturing's superior rapid prototyping capabilities. To visualize, test, and validate design concepts, prototyping is an essential stage in the product development process. The capacity of Additive Manufacturing to create prototypes and complex shapes quickly and efficiently is very beneficial. It drastically cuts down on the expenses and time associated with conventional prototyping techniques. Therefore, one of the main uses of Additive Manufacturing that is propelling its acceptance across a range of industries, including consumer goods, healthcare, and aerospace, is prototyping.

Based on Vertical

Industrial Verticals to Increase in Volume owing to Widening Applications in Aerospace & Automotive

In 2022, the industry leader in terms of product category is industrial Additive Manufacturing. This supremacy is the result of numerous significant reasons. Systems for industrial Additive Manufacturing are the best option for sectors like aerospace, automotive, and healthcare since they are built for large-scale production, high performance, and precision. To satisfy the demanding requirements of these sectors, they provide cutting-edge features, including multi-material capabilities, high-speed printing, and improved quality control. Furthermore, post-processing capabilities are frequently included in industrial Additive Manufacturing equipment, which improves the effectiveness of the entire production process. Although desktop Additive Manufacturing is useful for small-scale projects and quick prototyping, industrial systems are essential for commercial, mission-critical, and large-scale applications, which further cements their dominance in the Additive Manufacturing market.

Based on Material

Polymer to Emerge as the Most Valuable Material due to their Weight Postproduction

In 2022, the polymers had a significant share and are presumed to witness significant growth over the coming years. There are numerous important causes for this supremacy. First off, a variety of industries, including consumer products, automotive, aerospace, and healthcare, can benefit from polymer-based 3D printing due to its cost and versatility. Because weight reduction is a top objective in industries like aerospace, polymer materials' low weight is essential. Furthermore, polymer 3D printing can produce complicated designs and complex geometries, which makes it appropriate for a variety of prototypes and final products. Although metal and ceramic materials are useful in specific applications, polymer materials are still the most popular option since they provide an affordable and adaptable solution for a variety of Additive Manufacturing requirements.

Based on Region

North American Region to be Dominant in Terms of Utilization due to Widening Availability of Highly Qualified Personnel

Because it adopted Additive Manufacturing technology early and widely, the North American area has dominated market growth. The existence of well-established sectors like aerospace, automotive, and healthcare has consistently fueled the need for applications involving 3D printing. Furthermore, the United States' strong network of universities, creative entrepreneurs, and government assistance has made a substantial contribution to the region's technological developments and market expansion. North America's dominance in the global Additive Manufacturing market has been further cemented by the availability of highly qualified personnel and a robust network of Additive Manufacturing service providers.

Conversely, the Additive Manufacturing industry is expanding quickly in the Asia Pacific area. The region's rapidly expanding industrial sector, particularly in nations like China and Japan, is responsible for this expansion. These nations have taken use of Additive Manufacturing's potential to improve their production capacities and obtain a competitive advantage in the international market. Asia Pacific is becoming a popular destination for companies wishing to use Additive Manufacturing for mass production and customized items because of the region's comparatively cheaper production costs. As a result, the Asia Pacific region has emerged as a critical hub for the worldwide Additive Manufacturing market, and it continues to grow at a rapid pace.

Competitive Landscape

The market for Additive Manufacturing is highly competitive, with both well-established companies and creative newcomers present. Stratasys, 3D Systems, and EOS are just a few of the industry heavyweights that lead the way with a vast array of industrial-grade 3D printing solutions. With cutting-edge technology, upstarts like Desktop Metal and Carbon are becoming more popular. Active material providers that support material innovation include HP and BASF. Furthermore, design and simulation tools are provided by software suppliers like Siemens and Autodesk. In this quickly expanding sector, cooperation between hardware, software, and material firms is defining the competitive dynamics that are changing and placing an emphasis on integration and all-encompassing solutions.

The key players in the global Additive Manufacturing market include - Stratasys Ltd. (Israel), Materialise NV (Belgium), EnvisionTec Inc. (Germany), 3D Systems Inc. (U.S.), GE Additive (U.S.), Autodesk Inc. (U.S.), Made in Space (U.S.), Canon Inc. (Japan), Voxeljet AG (Germany) among others.

Recent Market Developments

- August 2022: Covestro AG, a supplier of Additive Manufacturing materials, was bought by polymer 3D printing startup Stratasys. Novel materials are adept at generating fresh applications for 3D printing, especially when it comes to manufacturing final products like orthodontic braces and auto parts. Stratasys can further its business objective of offering the best and most comprehensive polymer 3D printing portfolio in the industry with this acquisition. Additionally, the business can increase the rate at which it invests in innovative 3D printing material innovations.

- August 2022: Additive Manufacturing software provider ParaMatters was bought by Carbon. The acquisition will enable Carbon's product development teams to use this software's automated approaches to design parts with improved performance in less time. These designs will have enhanced performance attributes and sophisticated geometry.

Segmentation of the Global Additive Manufacturing Market

| Parameter | Details |

|---|---|

| Segments Covered |

By Component

By Printer Type

By Technology

By Software

By Application

By Vertical

By Material

By Region

|

| Regions & Countries Covered |

|

| Companies Covered |

|

| Report Coverage | Market growth drivers, restraints, opportunities, Porter’s five forces analysis, PEST analysis, value chain analysis, regulatory landscape, technology landscape, patent analysis, market attractiveness analysis by segments and North America, company market share analysis, and COVID-19 impact analysis |

| Pricing and purchase options | Avail of customized purchase options to meet your exact research needs. Explore purchase options |

FAQ

Frequently Asked Question

What is the global demand for Additive Manufacturing in terms of revenue?

-

The global Additive Manufacturing valued at USD 14.5 Billion in 2022 and is expected to reach USD 69.3 Billion in 2030 growing at a CAGR of 21.6%.

Which are the prominent players in the market?

-

The prominent players in the market are Stratasys Ltd. (Israel), Materialise NV (Belgium), EnvisionTec Inc. (Germany), 3D Systems Inc. (U.S.), GE Additive (U.S.), Autodesk Inc. (U.S.), Made in Space (U.S.), Canon Inc. (Japan), Voxeljet AG (Germany).

At what CAGR is the market projected to grow within the forecast period?

-

The market is project to grow at a CAGR of 21.6% between 2023 and 2030.

What are the driving factors fueling the growth of the market.

-

The driving factors of the Additive Manufacturing include

- Prototyping, Product Development, Innovation, And Time-To-Market

Which region accounted for the largest share in the market?

-

North America was the leading regional segment of the Additive Manufacturing in 2022.